preferred on

Analysis of Strategy’s STRC Preferred Stock and Bitcoin Acquisition Dynamics

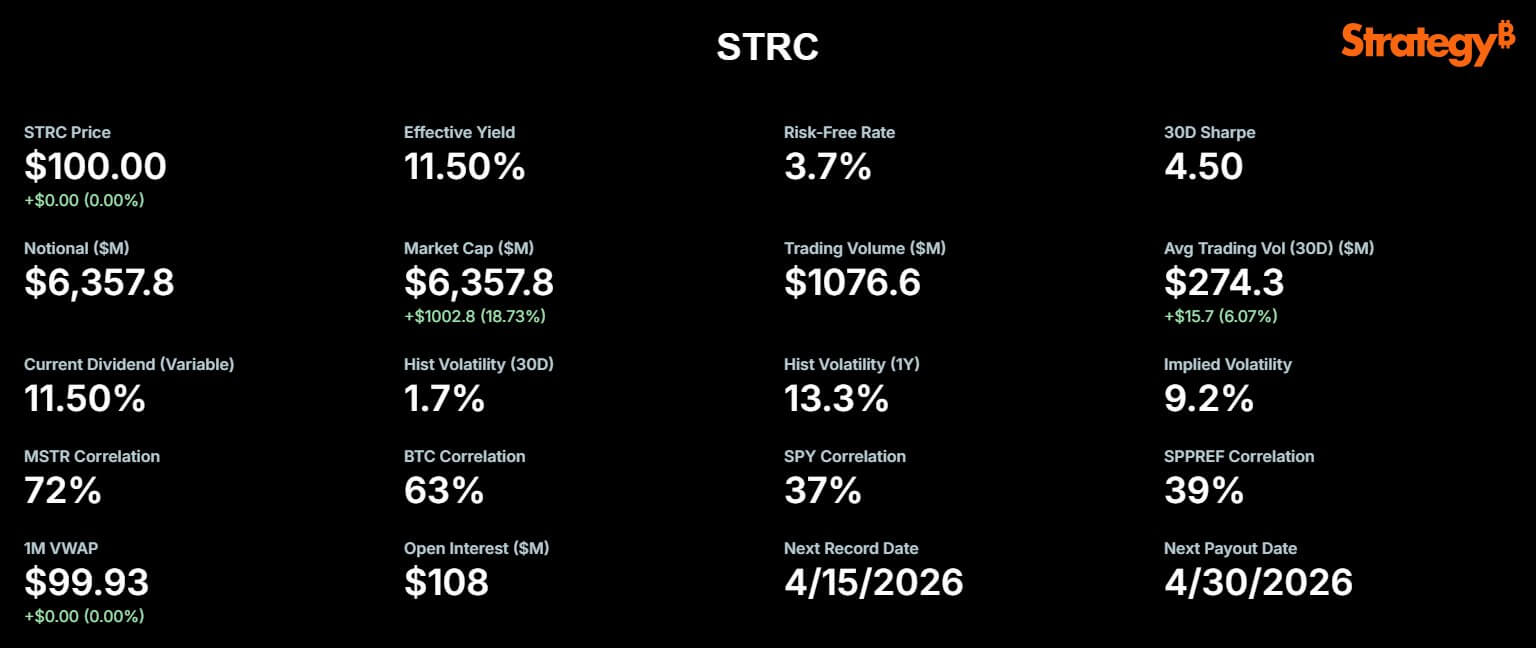

In a notable development within the cryptocurrency and financial markets, Strategy’s perpetual preferred stock, denoted as STRC, emerged as a pivotal instrument in the company’s strategic initiative involving Bitcoin. This week, STRC witnessed an unprecedented daily trading volume exceeding $1.1 billion, underscoring its significance in capital markets.

Key Developments and Market Reactions

On April 13, Strategy publicly announced that this date would serve as the record date for STRC, a communication made via a post on social media platform X. Notably, Michael Saylor, the company’s executive chairman, highlighted that the security concluded trading at par with only a marginal volatility of one penny, despite an impressive liquidity influx of $1.156 billion.

This surge in trading activity was catalyzed by Strategy’s announcement regarding the acquisition of 13,927 Bitcoin at an approximate expenditure of $1 billion between April 6 and April 12. As a result of this strategic move, the company now possesses a total of 780,897 Bitcoin, cumulatively acquired for a staggering investment of $59.02 billion, reflecting an average purchase price of $75,577 per coin.

Capital Structure and Financial Implications

Strategy disclosed that this substantial Bitcoin acquisition was entirely financed through at-the-market (ATM) sales of approximately 10.02 million STRC shares, yielding around $1 billion in net proceeds. This confluence of robust trading activity in STRC along with substantial weekly Bitcoin purchases funded solely through the preferred stock program signifies a marked shift in the company’s operational focus.

For equity investors, this transition could substantially recalibrate the risk-reward paradigm associated with their holdings. The increased reliance on preferred stock has the potential to mitigate immediate dilution effects for common shareholders due to the reduced issuance of ordinary shares in the short term. However, this strategy introduces fixed claims ahead of equity within the capital stack, prioritizing preferred shareholders for dividend distributions before common shareholders may receive any returns. Consequently:

– Preferred shareholders are entitled to dividends prior to any distributions being made to common shareholders.

– This structure inherently increases reliance on consistent market access and disciplined management of dividends.

– While such a paradigm could amplify returns should Bitcoin appreciate significantly, it concurrently elevates financial leverage and execution risks for common shareholders over time.

Mechanics and Strategic Intent of STRC Preferred Stock

The introduction of STRC in July 2025 signifies a strategic departure from Strategy’s existing MSTR common stock framework. The structure of STRC is characterized by its variable annualized dividend rate—currently set at an attractive 11.50%—which is deliberately designed to foster trading activity in close proximity to its $100 par value.

This pricing stability facilitates the efficient utilization of Strategy’s ATM issuance program. By issuing new STRC shares at a relatively consistent price point, the company can rapidly mobilize capital towards Bitcoin acquisitions while minimizing friction typically associated with large secondary offerings.

Market analysts have observed that STRC endeavors to provide investors with double-digit returns alongside minimal price volatility, effectively merging high-yield income with capital stability. Michael Saylor encapsulates this sentiment succinctly:

“STRC delivers money market-like stability with market-leading risk-adjusted returns.”

Since its inception, STRC has been instrumental in financing the acquisition of nearly 70,000 Bitcoin. The recent surge in trading volume on April 13 could potentially facilitate the acquisition of an additional 6,000 BTC.

STRC’s market capitalization has experienced significant growth alongside its utility—nearly doubling from $3.4 billion in February to approximately $6.36 billion presently. Furthermore, with an authorization for future issuances valued at $21.6 billion worth of STRC shares still available, the scope for additional Bitcoin accumulation appears substantial.

Concerns Regarding Financial Sustainability and Risk Factors

Despite prevailing market optimism surrounding Strategy’s operations and strategic initiatives, numerous analysts have voiced apprehensions pertaining to the sustainability of this financial model as articulated through the company’s own disclosures.

The software division of Strategy does not generate sufficient operational cash flow to meet its financial obligations; consequently, a reserve fund amounting to $2.25 billion was established in early February as a financial safety mechanism intended to cover approximately two-and-a-half years’ worth of dividend payments on preferred stock as well as interest obligations on outstanding debt.

This reserve is deemed essential because inadequate business income compels the company to rely on this cash set-aside to fulfill fixed payment obligations. Should this reserve become depleted prior to generating sufficient new revenue or identifying alternative financing sources, Strategy might confront exigent pressures necessitating asset liquidation or additional share issuance—circumstances that would jeopardize both preferred and common shareholder interests.

Critics contend that while such a reliance on ongoing market access may appear stable under current conditions, it could become precarious should financing environments shift adversely.

Independent Bitcoin analyst Derin Olenik recently published an incisive critique concerning the company’s obligations, articulating concerns regarding the unsustainable nature of current ATM growth rates. According to Olenik’s assessments:

– The obligations associated with STRC are escalating at an alarming compound monthly growth rate estimated at roughly 30%.

– Should this trend persist, the company’s liabilities could potentially double every three months and increase tenfold within one year—an acceleration that would dramatically heighten pressures on cash flow and existing reserves.

– Olenik projects that under these conditions, Strategy could exhaust its $2.25 billion reserve within a mere nine to ten months rather than over two-and-a-half years.

– To rectify such a deficit without resorting to Bitcoin liquidation would necessitate significant dilution of common shareholders’ stakes.

– Even if MSTR recovers to its historical peak valuations, projections suggest that up to one billion new shares may need issuance solely for servicing preferred dividends—resulting in an approximate dilution effect nearing 400% for existing common equity holders.

In conclusion:

> “If ATM issuance halts, Bitcoin accumulation stops. If issuance continues, the math dictates hyper-dilution regardless of stock price dynamics. From a common shareholder’s standpoint, STRC should not be perceived as Digital Credit but rather Digital Kamikaze.”

Support Perspectives: MSTR Bulls Advocating for STRC Viability

Conversely, proponents within Strategy’s investor base contest the pessimistic narrative articulated by Olenik. They assert that Strategy has effectively engaged a distinct investor demographic comprising income-seeking buyers who are amenable to accepting fixed claims coupled with limited upside potential associated with STRC.

By channeling proceeds from these conservative investors into high-volatility assets like Bitcoin—which possess significant long-term appreciation potential—Strategy ensures continued exposure for common shareholders while providing preferred investors with yield-focused instruments that exhibit characteristics more akin to short-duration credit rather than typical cryptocurrency proxies.

– **Short-Duration Credit Defined**: Such investments typically mature within five years or less and are characterized by lower sensitivity to interest rate fluctuations and expectations for principal return in shorter time frames.

– As such, STRC exhibits greater stability and predictability in trading patterns compared to typical cryptocurrency price movements.

It is noteworthy that Strategy consistently refers to STRC as its flagship “Digital Credit” instrument.

Analyst Adam Livingston remarked:

> “[STRC] is a machine that converts capital markets access into long-duration Bitcoin exposure while ensuring that fixed claims diminish relative to asset appreciation as BTC compounds.”

Supporters posit that this model remains viable provided Bitcoin appreciates at rates surpassing those required for servicing preferred dividends.

Under these assumptions, each successful issuance of STRC effectively transforms capital market demand into additional Bitcoin holdings while concurrently ensuring that fixed claims diminish relative to overall asset value as Bitcoin appreciates over time.

Michael Saylor has sought to reassure apprehensive investors by stating:

> “Our BTC Breakeven Accounting Rate of Return (ARR) is approximately 2.05 percent. If Bitcoin appreciates beyond this threshold over time, we can sustain our dividend obligations indefinitely without necessitating new MSTR share issuances.”

The Critical Lens: Evaluating Long-Term Implications for MSTR Common Shareholders

For holders of MSTR shares, paramount considerations center around whether this funding model will remain accretive over extended periods.

In the immediate term, evidence appears favorable; STRC experienced record turnover levels and consistently maintained par values while facilitating a considerable $1 billion Bitcoin purchase within just one week.

Such outcomes bolster management’s assertion regarding STRC’s capability as a reliable funding channel rather than merely serving as a transient financing mechanism.

However, examining longer-term implications reveals inherent complexities:

– Each successful issuance round adds layers of fixed claims above common stock.

– Strategy’s disclosures acknowledge potential dilution risks associated with future preferred share issuances and articulate concerns regarding adverse shifts in financing conditions which may impede maintenance of requisite dividend reserves.

Thus:

– **Dilution Defined**: This phenomenon occurs when new shares are issued resulting in diminished ownership percentages for existing shareholders—thereby decreasing their claims over corporate assets and profits.

– **Financing Conditions Importance**: The ability to secure affordable or stable funding is critical; failure here could hinder efforts required for adequate capital raising needed for dividend payments or structural maintenance—heightening overall risk profiles for both preferred and common stakeholders.

Ultimately, while STRC presents both robust opportunities and inherent risks—it operates effectively by attracting substantial liquidity while maintaining prices closely aligned with par values.

Nonetheless:

– This approach engenders potential tensions; each issuance further entwines broader strategic hypotheses concerning Strategy’s capacity to sustain market access while preserving dividend support alongside maintaining sufficient Bitcoin valuations justifying its comprehensive financial architecture.