preferred on

Overview of Ethereum Foundation’s Treasury Strategy Evolution

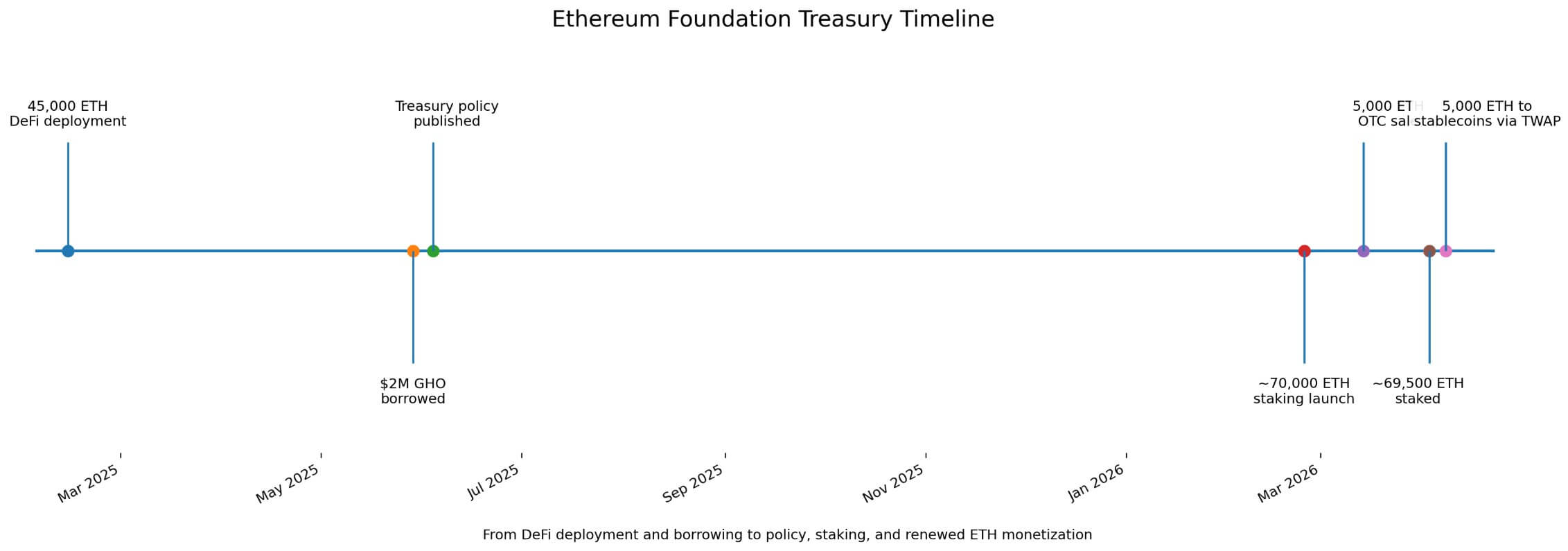

The Ethereum Foundation (EF) disclosed on April 8, 2026, its strategic decision to convert 5,000 ETH into stablecoins utilizing CoWSwap’s Time-Weighted Average Price (TWAP) feature. This initiative aims to facilitate the funding of research, grants, and various donations. This announcement reignited a critical dialogue regarding the foundational objectives underpinning the treasury overhaul previously undertaken by the EF.

Over the past year, the EF has executed a series of significant financial maneuvers, including reallocating treasury assets towards decentralized finance (DeFi), securing loans against ETH collateral, and instigating a staking initiative encompassing approximately 70,000 ETH.

The treasury policy outlined in EF’s June 2025 report indicated an alternative operational model that intricately associated monetization strategies with a fiat-denominated operational buffer while maintaining the interplay between ETH sales, staking initiatives, and stablecoin borrowing within a cohesive treasury framework.

Recent Developments in Treasury Operations

On February 13, 2025, the EF Treasury reported the deployment of 45,000 ETH across various platforms including Spark, Aave Prime, Aave Core, and Compound. Subsequently, on May 29, it secured a loan amounting to $2 million in GHO against its position in Aave. This maneuver carried substantial symbolic significance as it exemplified the EF’s ability to leverage DeFi infrastructure for working capital acquisition without necessitating immediate sales of spot ETH.

By early April, public sentiment had begun to reflect this interpretation of events; a Reddit discourse suggested that the EF had ceased its selling activities. One user noted positively that “it’s good that they stopped selling,” indicating a shift in market narratives regarding EF’s treasury management.

Despite this burgeoning optimism among retail investors, it is evident that a more nuanced understanding of EF’s ongoing treasury operations is warranted; particularly following the April 8 conversion.

Continued Liquidation Activity

As the EF inaugurated its staking program on February 24, it committed to staking an initial sum of 70,000 ETH with all rewards redirected back to bolster its treasury. On March 14, it concluded an over-the-counter (OTC) sale involving 5,000 ETH at an average price of $2,042.96. Just before the April conversion announcement, on-chain activity indicated that approximately 69,500 ETH had been staked—demonstrating that both selling and staking strategies had been concurrently operational.

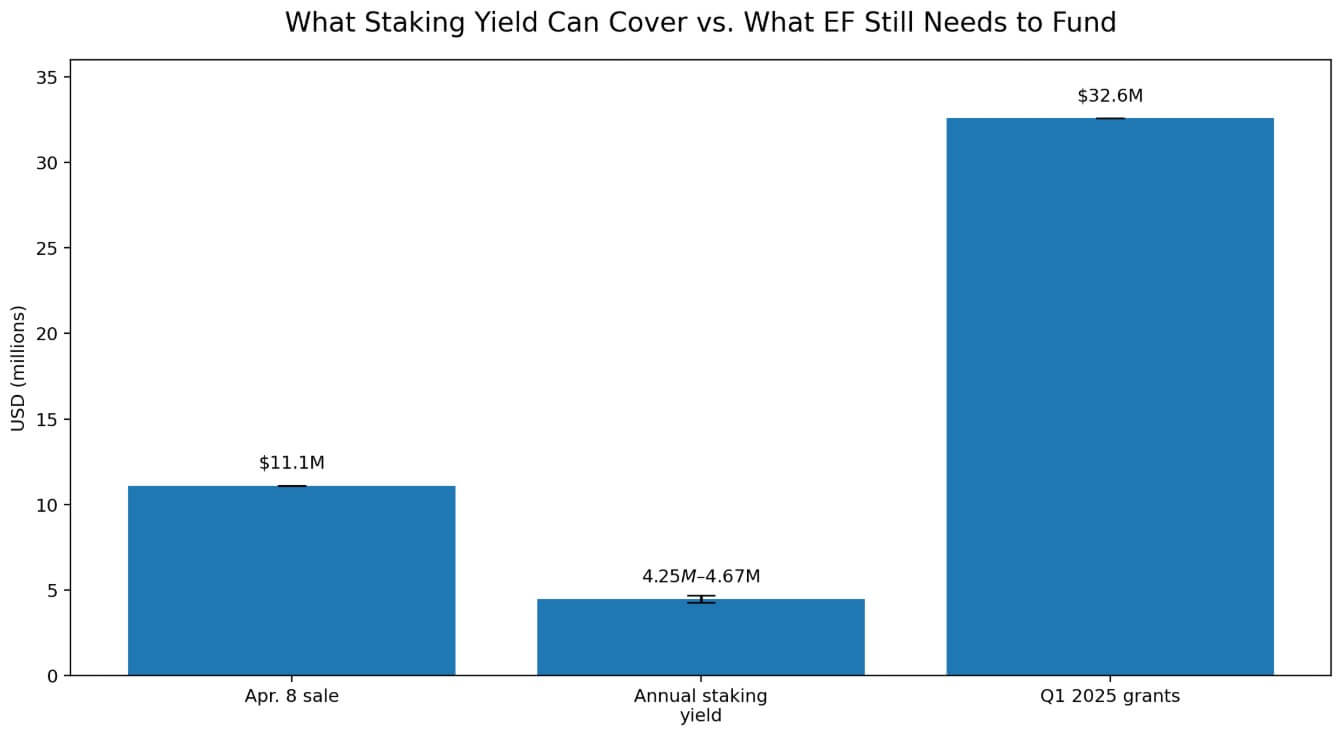

At an approximate ETH price of $2,220.76 during this period, this conversion translates into roughly $11.1 million in liquid capital. In contrast, staking yields for early April hovered between a rate of approximately 2.73% to 3.00%, equating to an annual yield between approximately $4.25 million and $4.67 million based on the full stake of 70,000 ETH.

Notably:

– The singular sale of 5,000 ETH represents approximately **2.4 to 2.6 times** the anticipated annual yield from the entire staking initiative.

The staking initiative enhances treasury efficiency while simultaneously diminishing funding requirements; nonetheless, it remains insufficiently scaled to entirely supplant treasury sales.

The EF’s June 2025 framework delineated an operational expenditure (opex) target at **15%** of total treasury assets with an operational buffer equating to **2.5 years**—thereby implying a fiat-denominated reserve target approximating **37.5%** of total treasury holdings.

When applied illustratively to EF’s last comprehensive treasury assessment from October 31, 2024—which reported total assets amounting to **$970.2 million**, including **$181.5 million** in non-crypto holdings—the policy would suggest a requisite reserve target nearing **$363.8 million**.

Following this snapshot period, EF publicly acknowledged further stablecoin exposure after deploying **2,400 ETH** along with approximately **$6 million** in stablecoins into Morpho in October of the same year. Additional announcements concerning further ETH-to-stablecoin conversions were made in subsequent months.

The precise dimensions of EF’s fiat-equivalent reserves remain somewhat nebulous; henceforth it is prudent to interpret the October report as an illustrative benchmark rather than an exact reflection of current financial standing.

The latest allocation update from EF revealed grant expenditure totaling **$32.6 million** for Q1 of fiscal year **2025**, translating into roughly **14,700 ETH** at current market prices. The conversion executed on April 8 only accounts for approximately **33%** of that quarter’s grant commitments and does not encompass contributions toward protocol research or staffing expenditures.

Yield generation combined with borrowing mechanisms permits maintenance of a fiat-centric budget yet necessitates periodic monetization efforts.

Potential Outcomes and Strategic Implications

The bullish outlook for EF hinges upon uncomplicated treasury arithmetic; a sustained increase in ETH prices combined with a reduced long-term opex ratio would empower the foundation to preserve its dollar buffer while necessitating fewer coin sales.

| Scenario | What Changes | Likely Treasury Effect |

|—————–|—————————————————-|———————————————————–|

| **Bull Case** | Increase in ETH price; decline in long-run opex ratio | Reduced need for coin liquidation |

| **Base Case** | Continuation of mixed strategies | Coexistence of staking rewards with periodic sales |

| **Bear Case** | Decline in ETH price; rising expenditure pressures | Necessitation for increased monetization |

| **Key Implication** | Reserve target remains fiat-denominated | “Less selling” narrative falters if ETH depreciates |

The aforementioned scenarios illustrate how staking rewards and judicious borrowing may serve to diminish quarterly sales pressures while affording EF greater latitude regarding transaction modalities—whether through OTC transactions or conservative utilization of DeFi protocols.

In this context, treasury modernization should manifest through diminished transaction frequency alongside enhanced execution quality.

Conversely, should adverse conditions prevail leading to price depreciation in ETH assets coupled with escalated spending pressures—EF may find itself compelled to liquidate more assets than previously anticipated to sustain operational viability particularly if it opts to exercise its counter-cyclical mandate by increasing spending during challenging market phases.

Under such circumstances, despite generating yield from substantial staked positions—the requirement for reserves could potentially escalate at a pace outstripping yield generation capabilities.

Public expectations surrounding a narrative favoring reduced sales may thus conflict with operational discipline codified within existing policy frameworks.

The April 8 conversion serves as a salient reminder of this discipline—a multifaceted strategy has already been deployed encompassing DeFi participation alongside stablecoin borrowing initiatives and selective asset liquidation efforts.

This evolving market narrative extends beyond mere policy articulation and reflects deeper dynamics inherent within the foundation’s operational ethos.