preferred on

Analysis of Bitcoin’s Current Market Dynamics

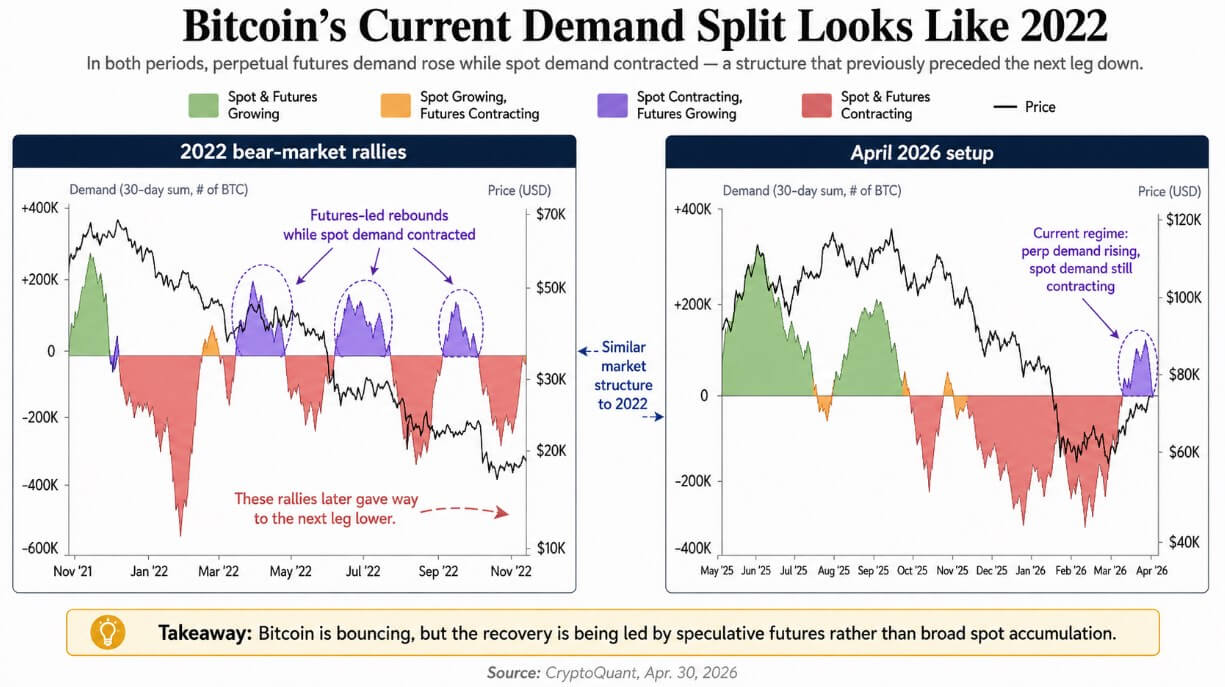

Recent insights derived from CryptoQuant’s analysis dated April 30, reveal a pivotal trend in the Bitcoin market, indicating that perpetual futures are emerging as the principal catalysts for Bitcoin’s recovery. This phenomenon occurs concurrently with a decline in spot demand, mirroring the market structure observed during the bear market rallies of 2022. Historical precedents indicate that leverage-driven price rebounds often culminate in subsequent downturns.

Understanding Demand Dynamics

In the cryptocurrency ecosystem, spot buying—facilitated through exchanges, exchange-traded funds (ETFs), or direct on-chain accumulation—represents a more stable form of capital commitment. Conversely, perpetual futures permit traders to engage in speculative positions utilizing borrowed capital, often at significant multiples of their original collateral, without necessitating ownership of the underlying asset.

The interaction between these two demand forms is critical: when both spot and futures demand expand synchronously, market rallies tend to be self-reinforcing. However, when futures activity leads while spot demand lags, the reliance on leveraged positions to finance price increases can result in forced liquidations should market conditions shift unfavorably.

Historical Context: The 2022 Bear Market Comparison

The dynamics of several bear-market rallies throughout 2022 exhibited analogous characteristics, with perpetual futures demand recovering prior to any signs of resurgence in spot demand. In these instances, while prices experienced temporary bounces driven by leveraged speculation, the underlying reality was that insufficient spot buying capacity led to inevitable sell-offs.

The current trajectory of Bitcoin as depicted by CryptoQuant re-establishes a condition wherein spot contracts are diminishing while futures contracts expand. This pattern raises concerns regarding market stability; specifically, it suggests that leveraged trading is gaining momentum before genuine cash demand materializes—circumstances that previously rendered price recoveries fragile during the last bear market.

Current Market Metrics

Recent data from CoinGlass reveals a stark contrast between Bitcoin’s futures and spot market volumes. As of April 30, the following metrics were recorded:

– **Bitcoin Futures Volume (24h):** $47.64 billion

– **Bitcoin Spot Volume (24h):** $4.07 billion

– **Futures-to-Spot Volume Ratio:** Approximately 11.7x

– **Open Interest in Futures:** Approximately $54.19 billion

This data underscores the dominance of derivatives activity within the market structure, raising potential concerns regarding liquidity and stability as forced liquidations could ensue from relatively minor price fluctuations due to high leverage levels available within perpetual futures contracts.

ETF Flow Dynamics and Market Sentiment

The recent flows from U.S. spot Bitcoin ETFs have further reinforced concerns regarding market structure. Notably, data from Farside Investors indicates aggregate outflows amounting to $490.5 million between April 27 and April 29. Such trends suggest a notable reduction in ETF bid activity coinciding with expanding futures positioning.

| Metric | Current Read | Significance |

|———————————————|————–|—————————————————|

| BTC Futures Volume (24h) | $47.64B | Indicates dominance of derivatives activity |

| BTC Spot Volume (24h) | $4.07B | Suggests a lack of robust support from spot demand |

| Futures-to-Spot Volume Ratio | 11.7x | Illustrates leverage-driven nature of current rally|

| BTC Open Interest | $54.19B | Indicates a substantial base of leveraged positions |

| US Spot BTC ETF Flows (April 27–29) | -$490.5M | Reflects recent volatility in ETF demand |

| IBIT Cumulative Net Inflows | ~$65.2B | Indicates sustained institutional interest |

| Total US Spot BTC ETF Cumulative Inflows | ~$58.1B | Suggests overall positive structural bid |

The cumulative net inflows associated with IBIT alone amount to approximately $65.2 billion, while total U.S. spot Bitcoin ETFs reflect approximately $58.1 billion in cumulative inflows—a marked contrast to the absence of structural demand witnessed during prior downturns.

The Bullish Perspective

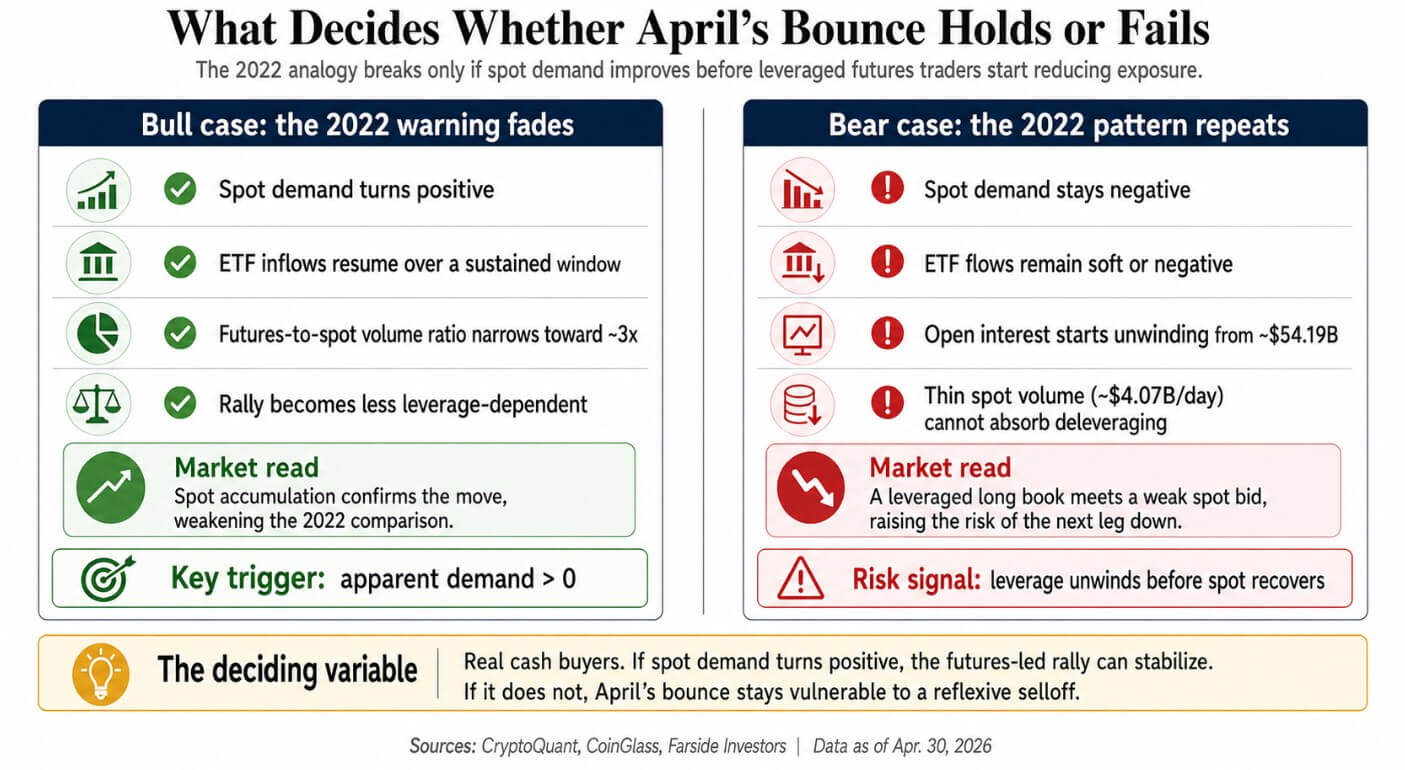

A divergence from the bearish narrative may emerge if spot demand begins to exhibit positive momentum prior to any reduction in leveraged exposure by traders. The observable uptick indicated by CryptoQuant’s demand metric surpassing zero would serve as a definitive trigger for validating a bullish case rooted in accumulated spot buying.

Structural Advancements Supporting Bullish Sentiment

The comparative analysis between current conditions and those observed in 2022 reveals several advancements beneficial for bullish sentiment:

– **Regulated U.S. Spot ETFs:** The advent of regulated ETFs introduces a layer of legitimacy and accessibility previously absent.

– **Enhanced Institutional Infrastructure:** A more profound institutional framework has developed over recent years.

– **Corporate Treasury Participation:** Sustained investments by corporate treasuries provide additional support.

Despite previous indicators of contraction in spot demand, there remains an acknowledgment that ETF and corporate purchasing behaviors have been accelerating. The bullish sentiment hinges on these entities increasing their purchasing activities sufficiently to elevate spot demand into positive territory once again.

The Bearish Considerations

The bearish perspective requires merely that leveraged traders begin reducing their exposure before any substantive improvement in spot demand occurs. Given that open interest currently stands at approximately $54 billion, even minimal unwinding could generate substantial selling pressure; coupled with the existing $4 billion daily spot volume, this scenario poses significant challenges for market stability.

This reflexive dynamic amplifies risk: declining prices may compel leveraged long positions toward liquidation, thereby exacerbating downward price movements and creating a feedback loop until adequate spot demand can stabilize prices effectively.

Ultimately, bear markets conclude upon simultaneous recovery within both spot and futures segments; however, given the present circumstance where futures are experiencing growth independently, Bitcoin mirrors the precarious structure reminiscent of 2022’s unsuccessful rallies.

The forthcoming weeks will be critical for determining whether this April’s rebound merely replicates previous failures or signifies a genuine shift—conditional upon either real cash buyers validating the futures-led price movement or observing the consequences of an inflated leveraged long position amidst insufficient support from spot demand.