A Comprehensive Analysis of Meta’s Strategic Re-Entry into the Stablecoin Ecosystem

The evolution of Meta’s engagement with the blockchain landscape has been marked by a series of significant milestones, commencing with the launch of its digital currency initiative, Libra, in 2019. This endeavor was subsequently rebranded as Diem before culminating in the divestiture of its blockchain assets to Silvergate Bank in 2022. The trajectory of these developments underscores the challenges presented by regulatory scrutiny and the withdrawal of banking partners, ultimately stalling what was initially a promising project.

Recent Developments in Creator Payouts

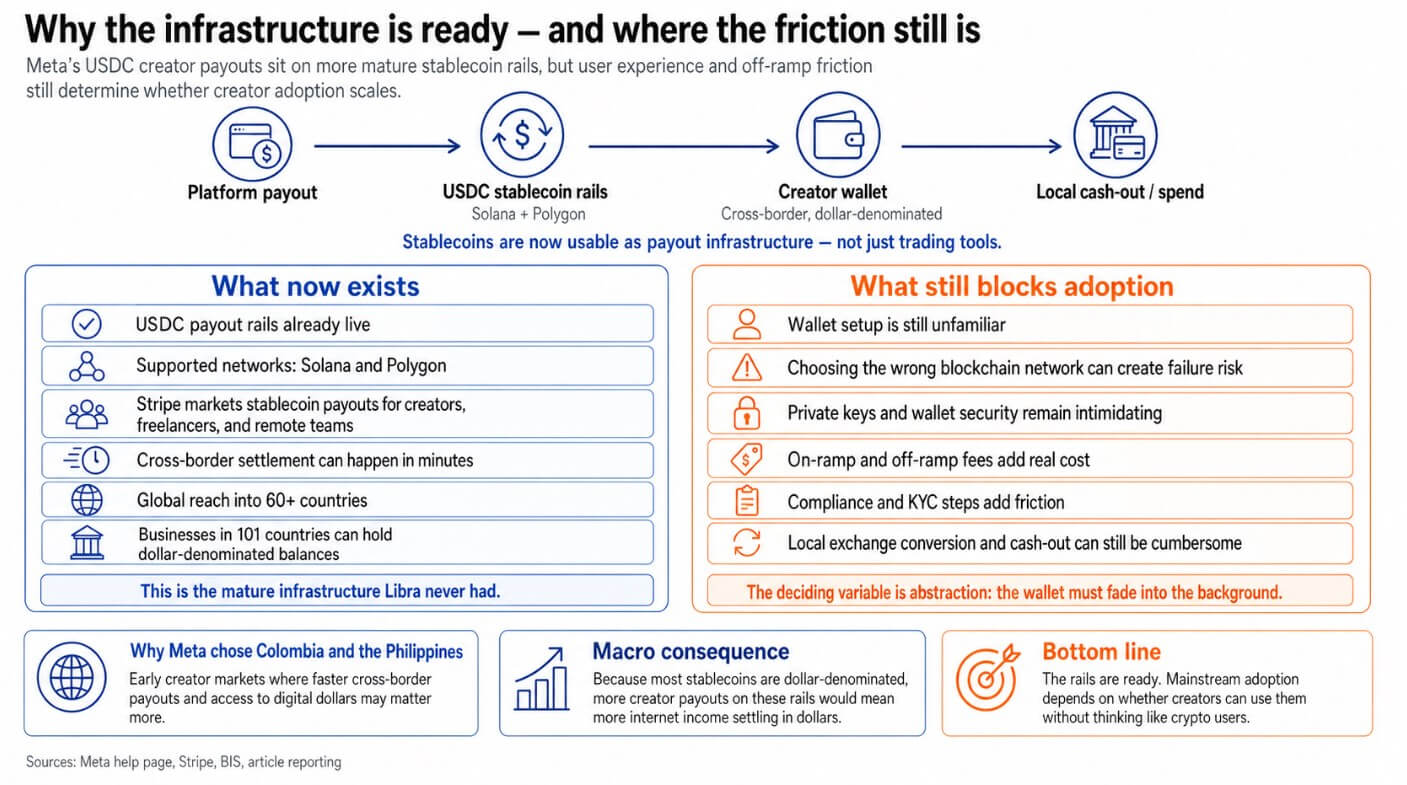

On April 29, 2023, Meta announced a groundbreaking initiative aimed at facilitating USDC payouts to eligible creators via compatible cryptocurrency wallets on the Solana and Polygon networks. This initiative is being piloted in select markets, notably Colombia and the Philippines, with initial participants being chosen from among local creators.

The strategic integration of creator payouts into existing dollar-stable frameworks—developed over several years by industry leaders such as Stripe and Circle—signifies a pivotal shift for Meta. The current deployment requires eligible creators to link a compatible wallet to directly receive USDC from Meta’s creator payout system.

The Economic Potential of the Creator Economy

According to an analysis conducted by Goldman Sachs, the creator economy’s valuation stood at approximately $250 billion in 2023, with projections estimating it could escalate to $480 billion by 2027. This expansive economic domain encompasses an estimated 50 million creators whose revenue streams are derived from various channels including brand partnerships, advertising revenue shares from platforms, subscriptions, tips, and direct payments.

Goldman’s findings suggest that brand collaborations alone constitute around 70% of creators’ overall revenue, indicating that a substantial portion of income traverses business-to-creator payment pipelines. To contextualize these figures:

- A 10% share of a $250 billion creator economy translates into an annual flow of $25 billion, or approximately $2.1 billion monthly.

- By 2027, assuming the same percentage holds true for Goldman’s projected $480 billion market size, this figure could rise to $48 billion annually or $4 billion monthly.

These Total Addressable Market (TAM) scenarios are contingent upon the broader payment flows within the creator economy and offer insight into the potential scale that this pilot project could reach, even with modest penetration rates.

Infrastructure Readiness for Stablecoins

The cessation of Libra was partially attributable to the absence of scalable stablecoin infrastructure at that juncture. However, significant advancements have since been made. Stripe has begun explicitly marketing stablecoin payouts as viable solutions for creators, freelancers, and remote teams. The adoption of USDC on networks such as Solana and Polygon—corresponding with Meta’s choices—demonstrates a concerted effort towards integrating stablecoin functionality within mainstream payment systems.

Stripe asserts that cross-border payments facilitated through stablecoins can be settled in mere minutes. Notably, businesses in over 101 countries previously unsupported by Stripe Treasury can now maintain dollar-denominated balances and transact across stablecoin rails seamlessly. The capability to process USDC payouts allows platforms to deliver payments to creators in Manila or Bogotá more efficiently than traditional wire transfers while ensuring transactions settle in U.S. dollars.

This rationale underpins Meta’s selection of Colombia and the Philippines as pilot regions; both markets exhibit burgeoning creator economies coupled with significant friction surrounding cross-border transactions and a pronounced demand for dollar-denominated savings options. Given that approximately 98% of stablecoins are dollar-denominated, any substantial increase in creator payouts via these channels would effectively contribute to the digital dollarization of the internet labor market—facilitating cross-border income settlements with minimal intermediaries involved.

Challenges to Adoption

Despite these advancements, challenges remain prevalent. Meta’s guidance materials assist creators in navigating compatible wallets and blockchain network choices; however, this process is far removed from the intuitive interfaces typically utilized by brand-deal creators without specialized knowledge.

Stripe has identified similar friction points: assets transacted across incompatible blockchains risk total loss without recourse; moreover, nominally low transaction costs may escalate when accounting for on-ramps, off-ramps, compliance burdens, and local currency conversion fees.

The Bank for International Settlements (BIS) highlights this broader issue by indicating that out of a projected $35 trillion in total stablecoin volumes by 2025, only approximately $390 billion will pertain to real-economy payments—a stark reminder that existing infrastructure has yet to achieve widespread adoption among mainstream consumers.

Potential Trajectories for Stablecoins within the Creator Economy

In an optimistic scenario (the “bull case”), rapid advancements in wallet abstraction could enable creators to receive USDC payments akin to receiving traditional Venmo transfers while ensuring that off-ramp processes are both economical and instantaneous across key markets.

This scenario would render the aforementioned 10% market share projection conservative; once major platforms normalize stablecoin payouts, ancillary services—including gig platforms and subscription tools—would be incentivized to adopt similar models.

Conversely, in a pessimistic outcome (the “bear case”), persistent wallet management complexities and off-ramp difficulties may inhibit widespread crypto-native adoption. In such a situation, Meta’s pilot program risks remaining a niche offering predominantly utilized by individuals already engaged with digital assets or operating within contexts where payout speed justifies existing managerial burdens associated with wallet maintenance.

| Factor | Bull Case | Bear Case |

|---|---|---|

| Wallet Experience | Wallet abstraction improves sufficiently so that receiving USDC becomes seamless for creators. | Creators continue grappling with wallet management complexities and security protocols independently. |

| Off-Ramp Quality | Off-ramp mechanisms evolve into cost-effective and swift solutions across crucial payout markets. | Cashing out remains cumbersome due to high costs or operational ambiguities. |

| Initial Adopters | Mainstream creators alongside gig workers begin adopting stablecoin payouts en masse. | Adoption remains confined predominantly to crypto-native individuals or users in high-friction corridors. |

| Payout Volume for Stablecoins | The anticipated 10% market share scenario appears conservative as more platforms incorporate similar options. | Payout volumes remain restricted and concentrated within limited pilot programs. |

| Impact on Real-Payments Share of Stablecoins | Creator payouts emerge as one of the premier non-trading categories for stablecoins, significantly enhancing real-payments activity. | Payouts remain overshadowed by trading activities with only marginal growth observed in real-economy applications. |

| Future Modeling of Meta’s Pilot Program | A successful model that prompts replication across various platforms catering to creators. | A specialized feature demonstrating infrastructure viability but insufficient mainstream traction. |

| Cross-Border Payout Efficiency | Dollar-denominated settlements meaningfully alleviate friction for creators operating in markets like Colombia and the Philippines. | Traditional payout methods retain greater familiarity and trust despite slower processing times. |

| Dollarization Impact | An increase in online income transitions onto dollar-backed stablecoin systems. | Dollar stablecoins remain peripheral rather than becoming standard payout mechanisms. |

| Main Constraints Faced | The primary challenge lies in execution and scalability of solutions offered. | User friction along with limited abstraction impedes broader acceptance. |

| Catalyst for Change | The emergence of invisible wallet experiences driving adoption alongside commercial growth. | The persistence of visible wallets as cumbersome elements deterring ordinary users from participation. |

Conclusion: The Importance of Abstraction in Adoption Dynamics

The contrasting trajectories outlined above underscore that abstraction will be a decisive variable influencing future adoption rates within this evolving ecosystem. Should wallet management complexities diminish significantly from user experience considerations—facilitating seamless transactions—the creator economy may indeed serve as a critical stress test for stablecoins’ viability within real-world applications. Conversely, if users remain encumbered by private key management and network choices, it is plausible that adoption will revert primarily to existing cryptocurrency users while relegating Meta’s pilot initiative to historical obscurity within industry narratives.