Over the past two years, discourse surrounding the integration of stablecoins into payment systems has predominantly concentrated on consumer behavior at the point of sale; specifically, the pivotal question arises: Will consumers ultimately opt for a digital wallet rather than a traditional card at checkout?

In response to these inquiries, industry giants such as Visa, Stripe, and Mastercard have mobilized substantial financial resources. Visa has commenced settlements in USDC, Stripe has strategically acquired Bridge, and Mastercard is in the process of acquiring BVNK.

These strategic maneuvers encapsulate a collective understanding that stablecoins are poised to serve as foundational layers for settlement and liquidity within established payment ecosystems. The entity that successfully commandeers this underlayer stands to dominate the economic frameworks governing forthcoming payment cycles.

According to Chainalysis, adjusted stablecoin transaction volumes are projected to reach $28 trillion by 2025, with optimistic estimates suggesting an escalation to an astonishing $719 trillion by 2035 based on organic growth trajectories. A more aggressive forecasting scenario posits that volumes could approach $1.5 quadrillion.

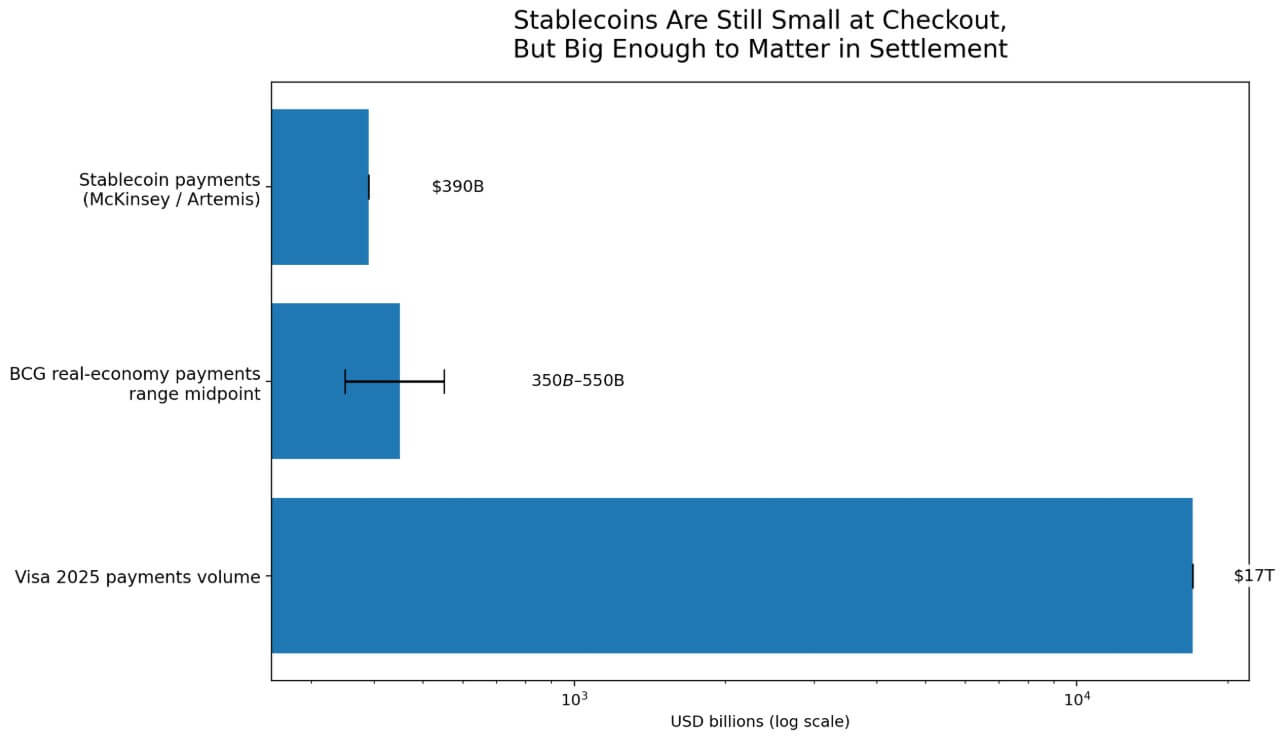

Further substantiating this perspective, research from McKinsey and Artemis estimates actual stablecoin payment volumes to be approximately $390 billion annually. This figure aligns closely with Boston Consulting Group’s estimation range of $350-$550 billion, excluding non-economic and speculative trading activities.

At these levels, stablecoins constitute roughly 2.3% of Visa’s projected $17 trillion payment volume by 2025. This relatively modest penetration rate holds the potential to recalibrate the economics surrounding settlement processes due to the disparate infrastructures underpinning settlement and checkout operations.

A significant proportion of hybrid stablecoin payment transactions may not manifest as on-chain merchant interactions. Transactions executed via crypto cards predominantly utilize conventional card rails, with blockchain technology capturing only issuer-related inflows and outflows. Consequently, a robust stablecoin settlement layer can proliferate commercially without necessarily being discernible at the point of sale.

Strategic Investments in Stablecoin Infrastructure

Visa initiated its USDC settlement operations within the United States in December 2025. By March 25, 2026, Visa had achieved an annualized run rate of $4.6 billion across over 130 stablecoin-linked card programs spanning more than 50 countries. The company’s strategic narrative emphasizes treasury modernization and enhanced settlement efficiency through its Canton Network initiative, which aims to expand these principles into payment processing, settlement mechanisms, and treasury applications for financial institutions. This initiative underscores Visa’s intent to seize control over the orchestration layer governing institutional stablecoin flows.

By March 2026, Bridge-enabled stablecoin-linked cards had been successfully launched in 18 countries, with aspirations to scale operations to over 100 countries by year-end. Concurrently, Visa is evaluating various options for settlement enhancement, expedited fund transfers, and simplified blockchain integration for institutional participants.

In its annual report published on February 24, 2025, Stripe disclosed a doubling of its stablecoin payments volume to approximately $400 billion, with an estimated 60% attributed to business-to-business (B2B) transactions. Moreover, it reported that Bridge’s transaction volume had quadrupled during this period. Stripe’s acquisition of Bridge received conditional approval from the Office of the Comptroller of the Currency (OCC) for establishing a national trust bank responsible for custody services, issuance management, orchestration processes, and reserve management.

Similarly, Mastercard’s agreement in March 2026 to acquire BVNK for up to $1.8 billion was coupled with an assertion that digital currency payment use cases had already reached a minimum of $350 billion in 2025. The incremental potential remains particularly significant within domains such as cross-border remittances, payouts, peer-to-peer transfers, and B2B transactions.

Mastercard has also highlighted speed and programmability as critical factors addressing treasury management challenges and commercial flow inefficiencies.

This collective movement among these three entities—Visa with its focus on USDC settlement; Stripe through its acquisition strategy; and Mastercard via its engagement with BVNK—reveals a unified thesis: the integration of stablecoin settlement mechanisms into existing payment infrastructures is occurring prior to any transformative revolution at the consumer checkout level.

| Company | Strategic Initiative | Implications | Main Use Cases | Control Point |

|---|---|---|---|---|

| Visa | Implementation of USDC settlement in the U.S.; Over 130+ stablecoin-linked card programs across 50+ countries; Expansion efforts via Canton Network | Treating stablecoins as integral components of treasury modernization and settlement infrastructure rather than mere checkout innovations | Merchant settlements; Treasury operations; Card issuance orchestration; Institutional settlements | Settlement + orchestration layer |

| Stripe / Bridge | Acquisition of Bridge; Stablecoin transaction volume reaching approximately $400B in 2025; Predominantly focused on B2B transactions (60%); Pursuing trust-bank status for custody services and reserve management | Establishing enterprise-level infrastructure for stablecoin transactions targeting business flows rather than solely retail-oriented crypto payments | B2B payments; Developer APIs; Custodial services; Issuance management; Enterprise infrastructure development | Developer/compliance stack |

| Mastercard / BVNK | Aquisition agreement with BVNK valued at up to $1.8 billion; Digital currency payment applications exceeding $350B+ in 2025 | Pursuing enhancements in cross-border payment capabilities while maintaining connectivity with fiat currencies through stablecoins | Cross-border remittances; Payouts; Peer-to-peer transfers; B2B payments; Treasury/commercial flow enhancements | Corridor distribution + commercial transactional flow management |

The Federal Reserve confirmed in an April 8 note that the market capitalization of stablecoins had reached approximately $317 billion as of April 6—an increase exceeding 50% since early 2025.

The enactment of the GENIUS Act by Congress in July 2025 marks a significant milestone by providing a formal legal framework essential for institutional adoption within the U.S. market.

Citi’s base case projection from September 2025 estimates that stablecoin issuance may reach approximately $1.9 trillion by 2030—a figure anticipated to support around $100 trillion in annual transactional activity while generating over $1 trillion in additional demand for U.S. Treasuries at that scale.

This current capitalization level of $317 billion signifies about 16.7% of Citi’s ambitious target for 2030—a stage advanced enough for major payment networks to dedicate capital but still nascent enough that future outcomes remain uncertain.

The Future Trajectory of Stablecoin Integration

The optimistic outlook hinges upon how swiftly compliance frameworks can assimilate stablecoin settlements at an enterprise scale. With regulatory clarity established through legislative measures such as the GENIUS Act—and both Visa and Bridge targeting expansion into over 100 countries by year-end—the landscape appears ripe for rapid development.

If enterprises begin adopting stablecoin settlements as routine components of treasury operations—encompassing cross-border payouts, merchant settlements, and B2B transactions—the migration towards on-chain rails could accelerate beyond any conservative forecasts currently available.

This scenario would render Citi’s projection of $1.9 trillion issuance as merely a baseline expectation while enabling firms that manage orchestration processes alongside compliance frameworks and reserves to capture significant economic advantages associated with this emergent financial architecture.

The pessimistic scenario posits that fragmented open stablecoin rails persist long enough for incumbent entities to absorb these functionalities into proprietary systems masquerading as unique features. The Federal Reserve’s observations from April 2026 highlighted vulnerabilities related to complex intermediation chains, vertical integration challenges, opacity issues, and risks associated with bank runs—factors that may propel regulated institutions towards favoring permissioned alternatives over open systems.

Citi’s research indicates that bank-issued tokenized money may surpass open stablecoins regarding institutional adoption—especially within corporate treasury management and capital markets where stringent compliance requirements could favor closed networks over more open alternatives. In such an outcome, while stablecoins continue their expansionary trajectory, economic benefits would largely accrue to regulated systems operating under permissioned frameworks whereby incumbents leverage stablecoins as functional elements rather than transformative solutions within their ecosystems.

| Scenario Type | Description of Outcome | Pervasive Economic Beneficiaries | Implications for Payment Systems |

|---|---|---|---|

| Bull Case Scenario | The utilization of stablecoin settlements becomes commonplace across treasury operations alongside cross-border payouts and merchant settlements incorporated into B2B flows. | Main players such as Visa, Stripe/Bridge, Mastercard alongside compliant infrastructure providers stand poised to benefit significantly. | The seamless integration positions stablecoins as default back-end rails supporting existing payment brands without disrupting front-end experiences. |

| Base Case Scenario | The adoption rate for stablecoins expands gradually within selective corridors alongside enterprise workflows while consumer-facing checkout experiences remain largely unchanged. | This scenario favors incumbent players augmented by a limited number of specialized infrastructure providers capable of accommodating ongoing demands. | A hybrid operational structure emerges combining traditional card systems alongside banks on front ends while reconciling increasing reliance on underlying stablecoin technologies. |

| Bear Case Scenario | The persistence of fragmented open stablecoin rails permits incumbents to leverage functionalities derived from cryptocurrencies merely as proprietary features integrated into their systems. | This outcome primarily benefits regulated incumbents deploying permissioned networks or alternative frameworks catering predominantly towards closed operational ecosystems. | |

Control Point Dynamics

| The decisive factors include orchestration capabilities along with compliance adherence alongside reserves management coupled with foreign exchange oversight alongside interoperability standards determining competitive advantage dynamics .

| < strong >Entities controlling back-end stack facilitate movement optimization instead of focusing solely on front-end checkout experiences .

| < strong >The pivotal focus transitions from ownership regarding card dominance towards asserting control over comprehensive money movement facilitation . | |

The Emergent Control Dynamics Among Payment Giants

The competitive landscape reveals distinct positioning strategies among Visa , Stripe , and Mastercard , each vying for primacy across various segments comprising back-end operational stacks . Visa aims toward achieving dominance through enhanced settlement mechanisms coupled with sophisticated card issuance orchestration capabilities . In contrast , Stripe along with Bridge emphasizes developer-focused APIs aiming toward B2B infrastructural frameworks coupled with regulation-compliant custodial services . Mastercard , meanwhile , concentrates efforts on optimizing cross-border corridors along remittance functionalities intertwined throughout commercial treasury applications .

This strategic positioning illustrates a shared perception among these industry leaders : The critical contest lies within realms comprising orchestration capacities , compliance adherence , reserves management strategies , foreign exchange operations alongside necessary interoperability standards shaping competitive paradigms moving forward .

Accordingly , projections from Chainalysis anticipate intersections between volumes pertaining toward off-chain transactions executed by Visa or Mastercard against burgeoning activity facilitated via emerging digital assets occurring between years spanning from **2031 through **2039 . Such intersections signify pivotal moments necessitating strategic shifts predicated upon evolving market dynamics . However , it is crucial not only to recognize these future trends but also appreciate how earlier inflection points will shape trajectories long before anticipated milestones arrive .

As industry players embark upon redesigning core settlement architectures revolving around innovative concepts like decentralized finance (DeFi) or blockchain-based tokens despite current limited market penetration below **3%** globally regarding traditional payment flows indicates profound implications ahead concerning those entities positioned favorably within compliance landscapes . Ultimately , those organizations able construct robust defenses around orchestration strategies while adhering closely towards evolving regulations shall determine who retains dominant control over lucrative economic opportunities emerging throughout this intersectional space .