Market Anticipations Surrounding Federal Reserve Rate Adjustments

In recent months, financial analysts on Wall Street have engaged in extensive deliberations regarding the timeline for potential adjustments to interest rates by the Federal Reserve. As of now, market participants are contemplating not only the possibility of rate cuts but also the feasibility of an imminent rate hike.

Current Market Sentiment Following Recent Fed Announcements

Following the Federal Reserve’s decision on March 18 to maintain its target interest rate range at 3.50%-3.75%, market dynamics shifted unexpectedly. As evidenced by Bloomberg-based pricing, the probability of a rate hike by October has surged above 60%, with approximately 15 basis points of tightening anticipated by that time. Additionally, the CME FedWatch tool indicates a near 40% likelihood of a rate hike by year-end.

Significantly, the probability of a rate cut occurring next month has plummeted from 17% in February to an astonishing 0% for April. Conversely, expectations for a hike have ascended to 6%. This divergence in market sentiment underscores a palpable disagreement regarding the timing and conviction behind such decisions; however, both indicators converge on a bullish outlook for rate hikes—a sentiment that had been dormant for several months.

The Role of Oil Prices in Market Dynamics

The catalyst propelling this renewed optimism is the dramatic uptick in oil prices. As of March 20, Brent crude surpassed $109 per barrel, while U.S. crude approached $98, largely influenced by escalating tensions in the Middle East that raise concerns over potential disruptions to the Strait of Hormuz—an essential chokepoint through which nearly 20% of global oil supply transits.

The Energy Information Administration (EIA) maintains a baseline forecast suggesting that Brent prices will decline below $80 per barrel by the third quarter and settle around $70 per barrel by year-end, provided that geopolitical disruptions abate. The current market sentiment appears to challenge this assumption, suggesting that traders perceive it as overly optimistic—this skepticism is significantly influencing rate expectations.

In response to these developments, the yield on the 10-year Treasury bond has climbed to approximately 4.37%, while the 30-year bond yield reached its highest level since September. Concurrently, the S&P 500 index is trending towards its fourth consecutive weekly loss.

Global equity funds experienced a significant outflow of $20.3 billion during the week ending March 18, with U.S. equity funds alone witnessing an exodus of $24.78 billion. In contrast, money market funds attracted $32.57 billion globally, illustrating a distinct shift in investor preference towards cash instruments yielding close to 4%, thereby incentivizing capital withdrawal from risk assets in real-time.

The Paradox Confronting Bitcoin as an Investment Asset

As of March 20, Bitcoin was trading just below the $70,000 threshold, reflecting a downward trend in tandem with major indices such as QQQ (-1.75%) and GLD (-1.93%). The very session that recalibrated Federal Reserve policy towards a more hawkish stance simultaneously applied downward pressure on gold prices—typically viewed as a safe-haven asset during geopolitical tensions—despite an environment that would conventionally bolster hard-asset hedges.

The price of gold decreased by 1.8%, attributed to rising yields and a strengthening dollar. This dynamic suggests that tighter financial conditions are exerting collective pressure on both gold and Bitcoin, thus overwhelming any potential safe-haven demand that might otherwise arise from geopolitical uncertainties.

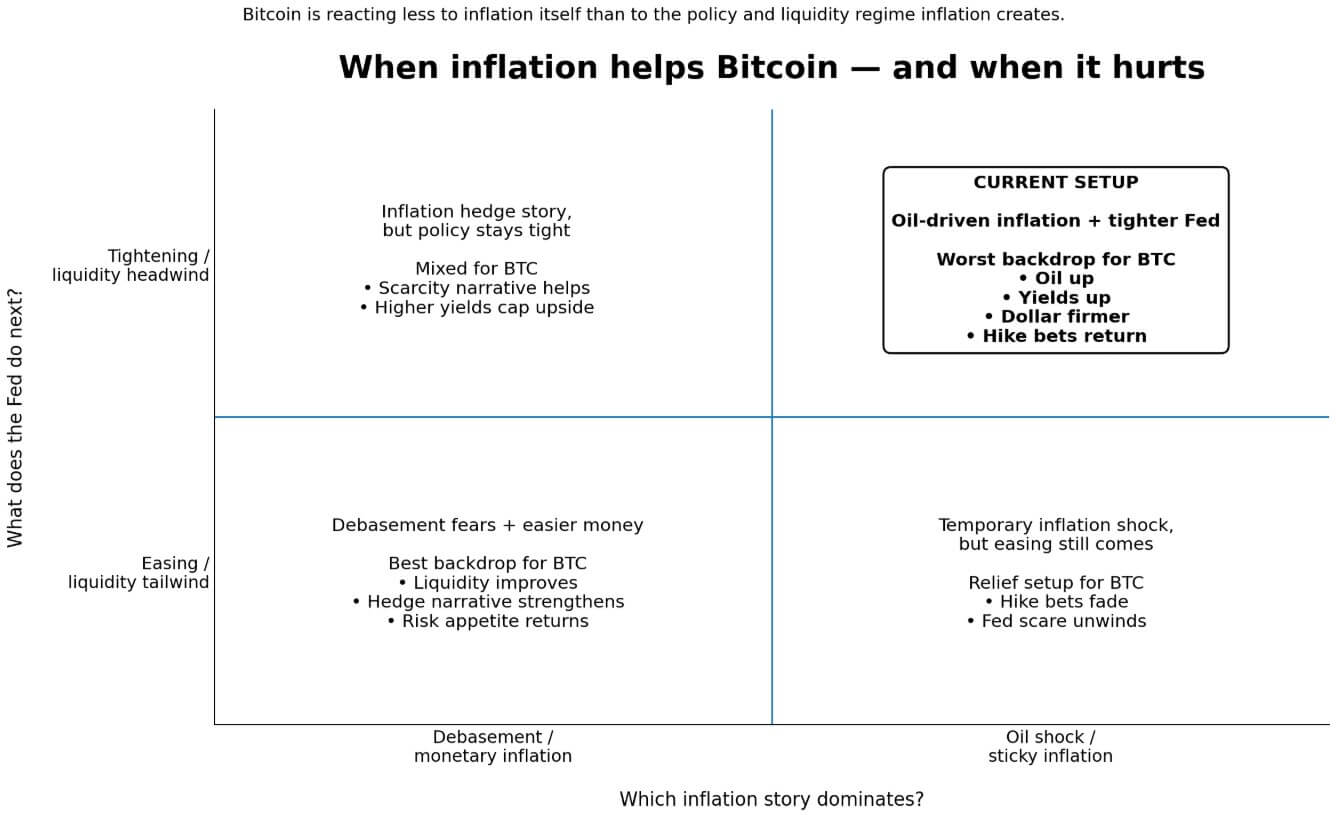

Bitcoin’s narrative as an inflation hedge encounters similar contradictions; while it usually thrives amid inflationary pressures signaling fears of currency debasement and potential monetary easing, it falters when inflation is driven upward by rising oil prices, increasing yields, and a stronger dollar—all while the Federal Reserve remains poised against easing measures.

Federal Reserve Chair Jerome Powell articulated at the conclusion of the March meeting that the central bank is closely monitoring whether increases in fuel and input costs will permeate core Personal Consumption Expenditures (PCE) inflation metrics.

If core inflation exceeds 3.2%, alongside unemployment rates stabilizing near 4.5% and oil prices remaining between $80-$100 per barrel, the Federal Reserve may find itself in a predicament where persistently high inflation necessitates maintaining restrictive monetary policies. Conversely, economic growth has not decelerated sufficiently to warrant emergency rate cuts; this creates a challenging environment for Bitcoin—one characterized by moderate inflation without recessionary pressures—potentially representing its most adverse macroeconomic backdrop.

An International Monetary Fund (IMF) working paper indicates that a singular factor related to cryptocurrency accounts for approximately 80% of price variability within this asset class; moreover, it posits that Fed tightening diminishes this factor through various risk-taking channels. Furthermore, as institutional capital increasingly enters cryptocurrency markets, Bitcoin’s correlation with broader equity markets has intensified.

The Bank for International Settlements (BIS) has documented Bitcoin’s recent downturn—approximately 50% from its peak values in early 2025—amidst a broader rotation away from growth-oriented assets following substantial declines in technology stocks.

The latest data from spot U.S. Bitcoin Exchange-Traded Fund (ETF) flows illustrates this shift: inflows peaked at $199.4 million on March 17 before transitioning into outflows totaling $253.7 million across March 18 and 19 combined, according to Farside Investors’ analysis.

Bitcoin’s valuation hinges upon which aspect of inflationary trends prevails: whether rising prices afford the Federal Reserve latitude for easing or compel it towards further tightening measures.

Potential Future Scenarios for Market Dynamics

The bullish case hinges upon adherence to EIA forecasts; should oil prices retract more swiftly than anticipated, labor markets soften ahead of the April 3 jobs report, and February’s PCE data slated for April 9 displays no second-round effects impacting core inflation measures, expectations surrounding rate hikes could dissipate just as quickly as they have ascended.

This week witnessed one-year inflation swaps reaching levels around 3%, while five-year forward swaps declined to approximately 2.35%, marking their lowest point in nearly one year. Such movements suggest market perceptions favoring a temporary energy disruption rather than an overarching regime shift.

Should this scenario materialize, Bitcoin could benefit from renewed liquidity support; Citigroup’s twelve-month framework posits a base-case target of $112,000 for Bitcoin with an aggressive bull-case target reaching up to $165,000 under conditions favorable to monetary easing initiated by the Fed.

| Scenario | Macro Trigger | Impact on Fed Expectations | Implications for Bitcoin |

|---|---|---|---|

| Bull Case | Oil prices retreat faster than anticipated; labor market softens ahead of April jobs report; February PCE data shows no secondary effects affecting core metrics | Hike probabilities diminish; markets shift towards pricing cuts or at least adopt a less hawkish Fed stance | BTC experiences liquidity tailwinds and begins trading more favorably based on easing prospects than tightening fears |

| Bear Case | Oil remains within an $80-$100 range into summer; core PCE inflation surpasses 3.2%; unemployment stabilizes near 4.5% | Hike probabilities solidify into a long-term higher-for-longer paradigm | BTC behaves akin to duration-sensitive risk assets as tighter financial conditions and enhanced cash competition exert downward pressure on price |

| Monitoring Metrics | April 3: jobs report; April 9: PCE data; April 28-29: FOMC meeting | Dissipating soft data would weaken hike narratives; persistent inflationary pressures and robust labor statistics would reinforce them | The outcomes of these reports will elucidate whether Bitcoin’s narrative as an inflation hedge regains legitimacy or if liquidity constraints deepen further |

The bear case predicates itself solely on inaccurate EIA forecasts; if oil sustains its position within the $80-$100 range throughout summer months and core PCE figures exceed thresholds set forth at 3.2%, coupled with statements from the April FOMC meeting endorsing market hawkishness rather than countering it, expectations for hikes will solidify into sustained positioning strategies.

Currently approaching record levels near $8 trillion, money market assets reflect investor wariness; flows redirected into cash during this tumultuous period may not spontaneously revert back into equities or riskier assets post-adjustments in sentiment. Under such circumstances, Citi projects Bitcoin could languish at around $58,000 as it trades under stringent financial conditions akin to duration-sensitive risk assets until interest rates stabilize or decline.

The Broader Global Context Influencing Monetary Policy

Brokers are now anticipating imminent hikes from both the European Central Bank (ECB) and Bank of England (BoE), with traders pricing in approximately 72 and 78 basis points of tightening respectively through to 2026. Furthermore, it is crucial to recognize that disruptions impacting oil flow through key trade routes like Hormuz also affect roughly one-fifth of global liquefied natural gas (LNG) trade; sustained interruptions could exacerbate energy costs across Europe and Asia concurrently and severely limit any major central bank’s capacity for easing monetary policy.

The heightened correlation between Bitcoin and global risk appetite—a phenomenon amplified by institutional engagement—indicates that tightening monetary policies may emanate from multiple fronts within a macroeconomic framework conducive to cryptocurrency appreciation.

Persistent containment of long-term inflation expectations continues to serve as a bulwark against potential stagflation scenarios; however, this containment does not negate pressing near-term policy implications necessitating scrutiny by market participants.

The Federal Reserve’s dot plot illustrates room for renewed hawkish sentiment: projections indicate appropriate rates ranging between 2.6% and 3.6% for participants through to 2026—the considerable dispersion at higher ends allows accommodation for one or two upward surprises in inflation metrics before median projections necessitate adjustment.

This juncture presents Bitcoin with a pivotal examination period—one that will ultimately determine whether it is regarded primarily as an inflation hedge or merely as a concentrated wager on global liquidity dynamics moving forward.