Market Dynamics: Bitcoin’s Pivotal Phase

Bitcoin is approaching a critical juncture wherein the market is poised to confront two divergent potential outcomes. Traders continue to incur costs in maintaining short positions; however, indicators related to price movement, exchange-traded fund (ETF) flows, and overall market leadership suggest that the prevailing sentiment may not align with a narrative of imminent collapse.

Current Market Sentiment and Funding Rates

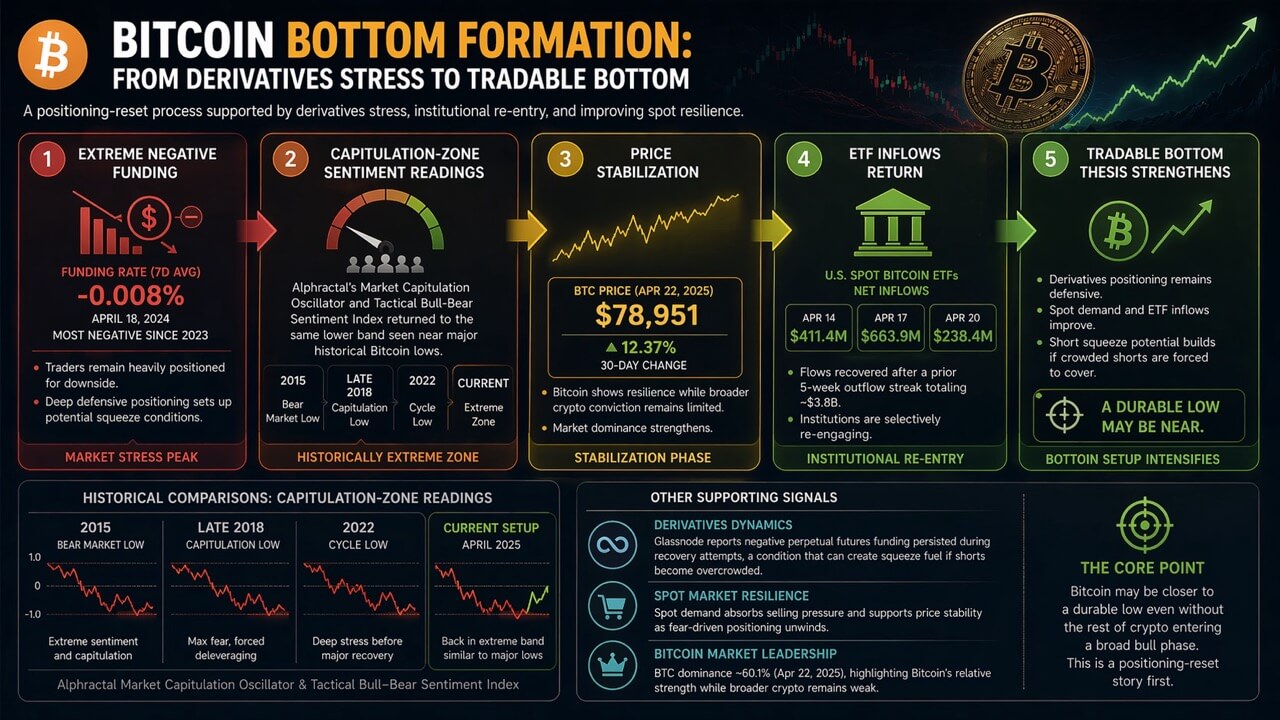

Recent analyses conducted by Alphractal have indicated that Bitcoin’s funding rates have reached their most negative levels observed since the inception of 2023. Their proprietary models have begun to signal a possible local bottom for Bitcoin, utilizing metrics such as the ‘Market Capitulation Oscillator’ and ‘Tactical Bull-Bear Sentiment Index.’ These indicators have entered an extreme zone historically associated with significant Bitcoin lows.

The accompanying chart illustrates that the sentiment index has consistently fallen into pronounced troughs during previous cycles, notably at pivotal moments such as the 2015 bear market nadir, the capitulation of late 2018, and the low experienced in 2022. The latest readings indicate that this index has once again returned to a lower band, reinforcing the assertion that market positioning has reached a notably stressed state.

This situational analysis suggests that Bitcoin is currently trading within a zone historically coinciding with capitulation events followed by subsequent reversals. Additional market data corroborates this perspective.

Funding Rates and Market Positioning

According to data from Crypto.com, the seven-day average funding rate declined to approximately -0.008% on April 18, marking its lowest level since 2023. Concurrently, Glassnode reported that negative funding persisted even as Bitcoin exhibited signs of stabilization and improved spot conditions. This peculiar market condition leaves Bitcoin at a crossroads:

- It may be emerging from a positioning washout conducive to a tradable rebound.

- Conversely, macroeconomic pressures that precipitated previous drawdowns may still possess sufficient strength to induce another substantial decline.

As of April 22, CryptoSlate reports Bitcoin’s price at $78,951, reflecting a 12.37% increase over the preceding thirty days, alongside a market dominance of 60.1%. While these conditions do not indicate an imminent broad speculative breakout, they do suggest an asset regaining leadership amidst a backdrop of limited conviction in other cryptocurrencies.

The Case for Market Reversal Gains Traction

The bullish narrative is increasingly supported by the resilience exhibited in spot demand while derivatives positioning remains cautious. Glassnode’s findings indicate that perpetual-futures funding has remained negative despite Bitcoin’s attempts at recovery from its recent downturn. Sustained negative funding can serve as a catalyst for upward price movement when short positions become overcrowded; however, it simultaneously reflects the prevailing caution among leveraged traders.

The nuances of this situation are further complicated by Bitcoin’s price behavior, which appears less tethered to a bearish liquidation scenario and more indicative of demand from buyers willing to counteract macroeconomic fears. Notably, one of the most significant channels for this demand has been the ETF segment. According to Farside Investors, U.S.-based spot Bitcoin ETFs witnessed inflows of $411.4 million on April 14, followed by $663.9 million on April 17, and an additional $238.4 million on April 20.

This pattern of inflows illustrates that substantial institutional capital did not dissipate during periods of heightened market tension. Moreover, this rebound appears credible as it follows an institutional reset characterized by a five-week outflow streak totaling approximately $3.8 billion from spot Bitcoin ETFs prior to early March’s recovery.

If this cautious re-engagement persists while funding rates remain negative or stabilize gradually, short positions could face greater vulnerability than current market sentiment suggests. This represents the most compelling iteration of the bottoming argument without necessitating assertions regarding the onset of a full-cycle bull market.

Macroeconomic Constraints on Market Potential

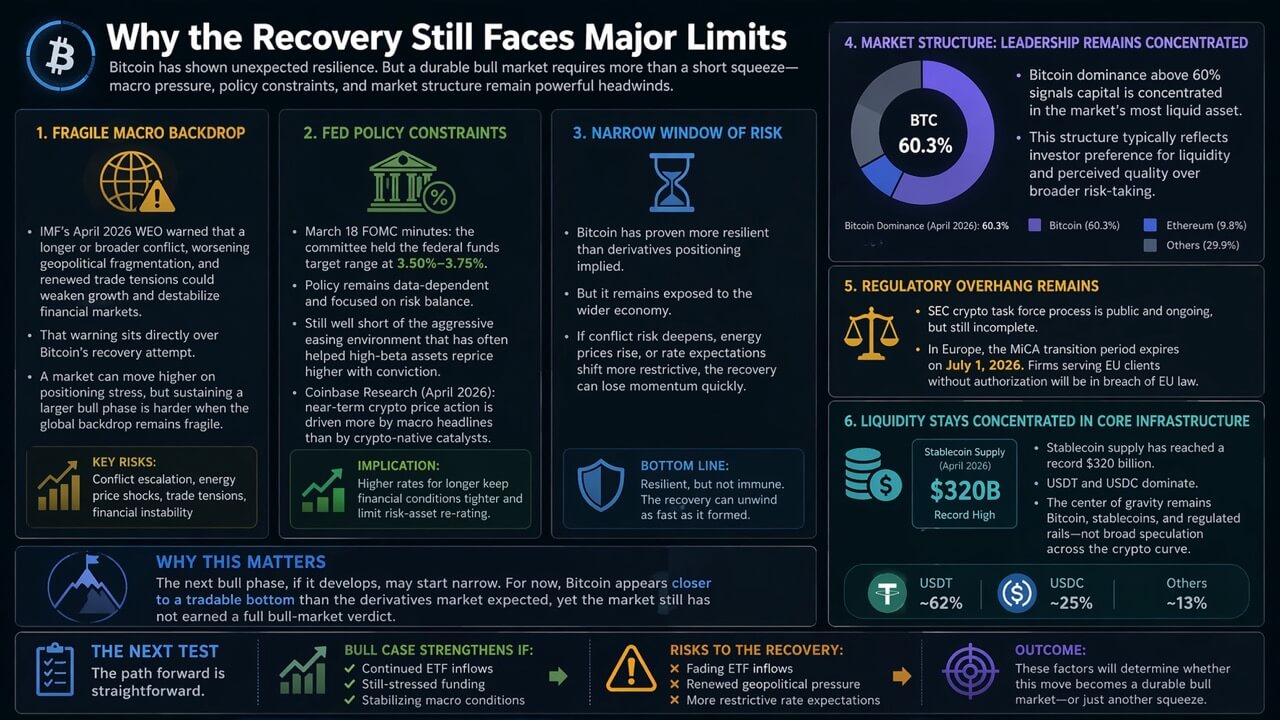

The ongoing assessment will determine whether tactical rebounds can evolve into broader and more sustainable growth trajectories; however, existing macroeconomic constraints are increasingly difficult to overlook. The International Monetary Fund (IMF) issued its April 2026 World Economic Outlook report highlighting risks associated with prolonged geopolitical conflicts, exacerbated trade tensions, and their potential ramifications for economic growth and financial market stability. These warnings coincide directly with Bitcoin’s current recovery endeavors.

A market can experience upward momentum driven by positioning stress; however, fostering a comprehensive bull phase is inherently challenging if the global macroeconomic landscape continues to deteriorate.

The prevailing interest rate environment further complicates this outlook. Minutes from the Federal Reserve’s March 18 meeting revealed that the committee maintained its federal funds target range between 3.5% and 3.75%, remaining attentive to incoming data and an evolving risk landscape. This stance diverges significantly from historical easing cycles known for facilitating substantial asset repricing based on investor conviction.

Coinbase Research’s April outlook aligns with this assessment, asserting that short-term cryptocurrency price movements are increasingly influenced by macroeconomic narratives rather than intrinsic crypto-specific catalysts. Thus, Bitcoin finds itself ensconced in a narrow yet pivotal window; while it appears more resilient than anticipated by derivatives traders, it does not seem insulated from overarching economic influences.

Prospects for Future Bull Phases

The structural dynamics of the broader cryptocurrency market argue against declaring an immediate onset of an expansive bull market phase. Bitcoin’s dominance exceeding 60%, as reported by CryptoSlate’s data analytics platform, underscores leadership concentrated in this most liquid asset class—a phenomenon typically observed when investors prioritize liquidity and perceived quality amidst heightened risk aversion.

This behavior aligns well with both current environmental conditions and regulatory frameworks. The U.S. Securities and Exchange Commission (SEC) maintains an active regulatory process regarding cryptocurrencies while European regulations are set to become more stringent post-July 1, 2026—marking an end to transitional periods under MiCA legislation. Such measures introduce a formalized environment contrasting sharply with previous periods characterized by looser regulatory oversight that facilitated earlier crypto rallies.

Simultaneously, liquidity within the cryptocurrency ecosystem remains robust; stablecoin supply has surged to unprecedented levels at $320 billion while USDT and USDC dominate liquidity streams despite ongoing legislative negotiations surrounding market structure in Washington.

This landscape indicates that the contemporary cryptocurrency zeitgeist is predominantly centered around Bitcoin and stablecoins—alongside regulated financial infrastructures—rather than showcasing broad speculative enthusiasm across diverse assets.

If a larger bull phase ultimately materializes, it may commence from this narrower base rather than unfolding uniformly across all risk dimensions within the crypto spectrum.

In summary, while Bitcoin appears closer to establishing a tradable bottom than anticipated by derivatives markets, it has yet to secure an affirmative verdict for entering a full-fledged bull market cycle. Alphractal’s sentiment index illustrates extreme lows adjacent to several significant Bitcoin troughs indicating that sentiment and positioning are once again situated within historically capitulative zones rather than typical corrective dips.

However, it is crucial to note that while descriptive charts substantiate qualitative patterns within these dynamics, they are insufficiently precise alone for confirming exact timing regarding local bottom formations within established time frames.

The forthcoming tests are unequivocal: should ETF inflows persist in building momentum amid negative funding or gradual normalization alongside stabilized macroeconomic conditions—the case for establishing a durable bottom will gain considerable strength. Conversely, should inflows diminish or geopolitical tensions intensify alongside restrictive rate expectations—the current recovery narrative may ultimately resemble merely a transient squeeze rather than initiating the first leg of a new bull market cycle.