preferred on

Market Response to Iran’s Announcement on the Strait of Hormuz

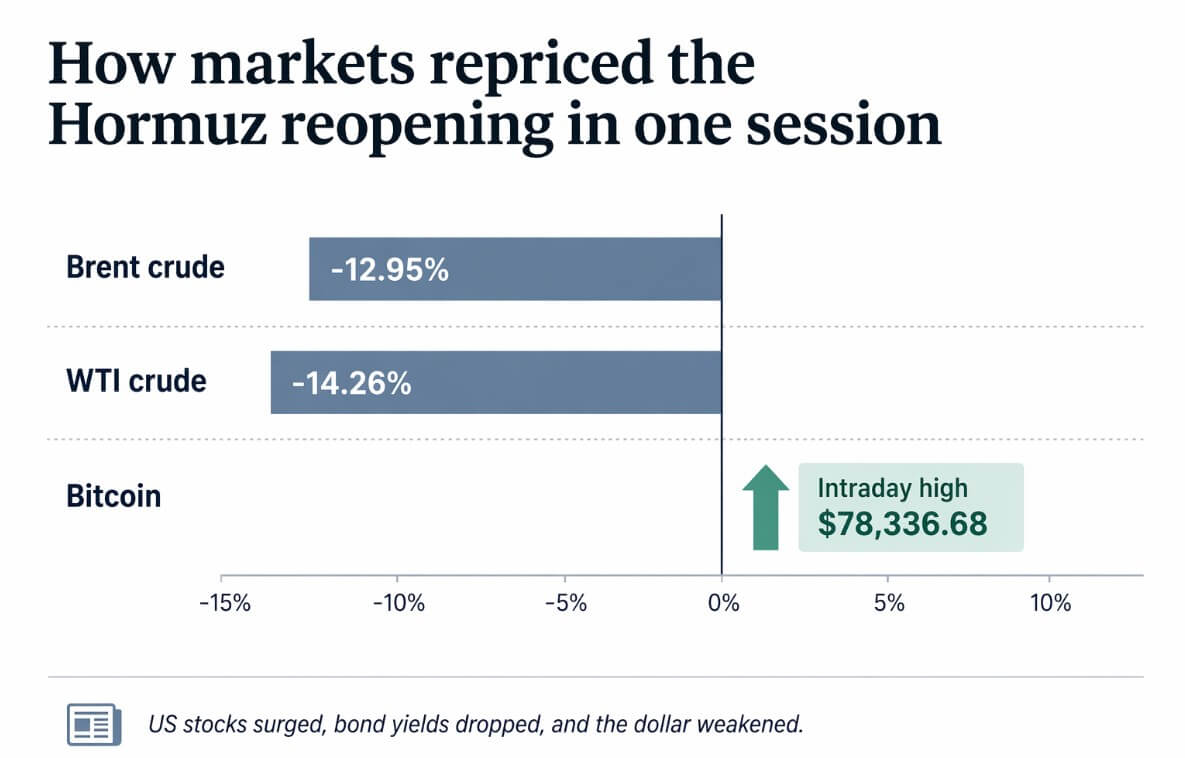

The recent proclamation by Iranian authorities regarding the temporary reopening of the Strait of Hormuz, coinciding with an ongoing ceasefire, has precipitated one of the most significant reversals in oil prices observed this year. Specifically, Brent Crude oil plummeted by 12.95%, settling at $86.52 per barrel, while West Texas Intermediate (WTI) experienced a more pronounced decline of 14.26%, reaching $81.19, marking their lowest valuations since March 11 and representing the most substantial single-day drops since April 8.

This sharp decline in oil prices catalyzed a robust rally in U.S. equities, accompanied by a concomitant decrease in bond yields, a depreciation of the U.S. dollar, and a notable surge in Bitcoin, which peaked at an intraday high of $78,336.

Traders effectively eliminated the “war premium” that had been incrementally infused into crude oil prices over preceding weeks, prompting a recalibration of risk assets across the board.

Operational Dynamics and Market Implications

As a result of Iran’s terms for reopening the Strait, commercial vessels are now mandated to obtain authorization from Iran’s Ports and Maritime Organization and the Islamic Revolutionary Guard Corps (IRGC), navigating through designated safe lanes. Notably, the U.S. blockade on Iranian shipping remains firmly intact until a comprehensive diplomatic resolution is achieved.

However, following these developments, Iran announced on April 18 that it had reinstated its closure of the Strait due to the persistence of the U.S. blockade, thereby reinstating market anxieties as the deadline for ceasefire negotiations approaches on April 22.

During this brief period of purported reopening, only eight oil and gas tankers successfully traversed the Strait, underscoring that operations have yet to return to any semblance of normalcy.

The Arithmetic of Fear: Supply Chain Vulnerabilities

According to data from the Energy Information Administration (EIA), average daily oil transit through the Strait is projected to reach approximately 20 million barrels by 2024, accounting for roughly 20% of global petroleum liquids consumption. A staggering 84% of crude and condensate exports and 83% of liquefied natural gas (LNG) are directed towards Asian markets. This statistic serves as a critical benchmark for market participants: unless shipping traffic resumes to pre-conflict levels before April 22, this vital route remains functionally impaired.

Impact Assessment: War-Induced Supply Losses

Since hostilities commenced, more than 500 million barrels of crude and condensate have been effectively removed from global supply chains, resulting in an estimated $50 billion loss in output. For context, global onshore crude inventories witnessed a decline of approximately 45 million barrels in April alone.

Prior to these developments, forecasts indicated Brent prices averaging $115 per barrel in Q2, with Morgan Stanley projecting similar figures. However, current pricing dynamics reflect an alarming deviation from these anticipated baselines.

The Fragility of Reopening Efforts

The operational parameters established by Iran on April 17 echo sentiments expressed earlier by Iranian officials regarding restricted maritime passage that has historically remained below 10% of normal traffic levels. The diplomatic landscape has shifted without altering fundamental operational realities; a ceasefire accompanied by renewed diplomatic engagements has led markets to misinterpret these conditions as de-escalation.

| Issue | Current Status | Significance |

|---|---|---|

| Commercial Passage | Allowed with Iranian coordination | Conditional passage remains possible |

| Authorization | Requires approval from Ports and Maritime Organization + IRGC | Centrality of Iranian control emphasized |

| Routing | Iran-designated safe lanes | No equivalent to standard freedom of navigation |

| IMO Standard | Not yet confirmed | Legal ambiguity persists |