Recent Japanese Currency Market Intervention: An Analytical Report

Recent developments in the global currency markets have garnered significant attention, particularly Japan’s reported intervention amounting to approximately $35 billion aimed at purchasing yen. This decisive action has precipitated a substantial depreciation of the U.S. dollar, which fell nearly 3% to a rate of 155.5 yen per dollar.

Contextual Background

The Bank of Japan (BOJ) has indicated through its money-market data that the aforementioned intervention figures are credible. The forthcoming confirmation from the Ministry of Finance’s monthly report will mark Japan’s inaugural official action to support its currency in nearly two years, potentially ranking as the second-largest intervention ever recorded.

The BOJ’s April economic outlook suggests that consumer price index (CPI) growth, excluding fresh food, is projected to range between 2.5% and 3.0% for fiscal year 2026. Moreover, economists anticipate a re-acceleration of inflationary pressures, primarily driven by escalating oil prices and the concomitant weakness of the yen, which exacerbate import costs.

It is noteworthy that approximately 95% of Japan’s crude oil imports traverse the Strait of Hormuz. The BOJ’s baseline scenario posits that Dubai crude oil prices will stabilize between $70 and $80 per barrel, contingent upon the absence of significant supply disruptions. The political tolerance within Tokyo for sustaining inflationary imports amidst a depreciating yen is finite—this limit appears to have been breached in recent days.

Monetary Policy Dynamics

On April 28, the BOJ maintained its policy interest rate at 0.75%, albeit with dissent from three board members advocating for a rise to 1%. Similarly, the Federal Reserve held its policy rate steady at a range of 3.50% to 3.75% on April 29.

This stark short-rate differential of approximately 275 to 300 basis points serves as a mechanical impetus for the resurgence of carry trades. The relative affordability of yen-denominated borrowing positions Japan favorably compared to global counterparts, while concurrently enhancing the appeal of investing in higher-yielding assets denominated in U.S. dollars.

It is essential to recognize that interventions executed without convergence in interest rates merely serve as a temporary reprieve. A Reuters poll conducted on April 16 revealed that 65% of economists anticipate that the BOJ will achieve a rate of 1.0% by the conclusion of June 2026, with additional hikes projected through 2027.

The Global Implications of Yen Weakness

The Bank for International Settlements (BIS) reports indicate that the yen constituted approximately 16.8% of all foreign exchange transactions globally as per its triennial survey conducted in 2025. Furthermore, an additional BIS study estimated that yen-funded carry trades were valued at approximately $250 billion prior to their unwind, while UBS approximated this figure closer to $500 billion, with only partial unwinding observed at that time.

A separate analysis from the BOJ elucidates that balance sheet expansions funded by yen liabilities are predominantly driven by hedge funds and financial intermediaries engaged in assets distanced from Japanese currency markets.

As evidenced by Commodity Futures Trading Commission (CFTC) positioning data from April 21, leveraged funds within CME yen futures held a total of 80,220 long contracts juxtaposed against 148,717 short contracts—indicative of an increase in gross shorts exceeding 16,000 week-over-week.

In scenarios where the yen experiences sudden appreciation, those holding short positions must seek coverage; this necessitates trimming their asset holdings funded by these trades.

| Metric | Bank of Japan | Federal Reserve | Implications for Carry Trade |

|---|---|---|---|

| Policy Rate | 0.75% | 3.50%-3.75% | The significant gap sustains low funding costs in yen and enhances returns on U.S.-denominated assets. |

| Date of Latest Policy Decision | April 28, 2026 | April 29, 2026 | This indicates an active divergence in monetary policy rather than historical shifts. |

| Current Short-Rate Gap | Approximately 275–300 bps | This differential is critical for motivating yen-funded carry trades. | |

| Policy Bias | Three dissenting BOJ board members advocated for a rate increase to 1.0% | Federal Reserve maintained current rates | This suggests gradual movement towards tightened policy in Japan; however, current conditions do not sufficiently narrow the spread. |

| Market Expectations | Reuters poll: Anticipation for BOJ reaching 1.0% by end-June 2026 | No immediate comparable shifts expected from Fed policy | A rate hike from BOJ could compress carry spreads and diminish attractiveness of short-yen positions. |

| Carry Trade Implication | Low-cost funding currency | Higher-yield destination market | This dynamic enables investors to cheaply borrow in yen while seeking superior returns elsewhere. |

| Article Takeaway | Interventions can influence FX markets; however, without interest rate convergence, they only postpone inevitable adjustments. | Elevated U.S. yields perpetuate carry trade incentives. | This explains why persistent weakness in the yen continues to arise and why abrupt rebounds may necessitate liquidations across risk assets—including Bitcoin. |

BIS data further indicates that foreign-currency credit denominated in yen contracted by approximately 4.9% during the year 2025; hence, it is plausible that the carry complex may be somewhat diminished, thereby reducing the mechanical impetus for any potential unwinding actions.

The intricate relationship between Bitcoin and global leverage is underscored by margin calls and risk appetites prevalent among macro funds engaged simultaneously in short-yen positions and long higher-yielding assets. A review published by BIS in August 2024 revealed that procyclical deleveraging coupled with margin increases exacerbated shocks across risk assets; notably, Bitcoin plummeted by approximately 13% during this tumultuous period.

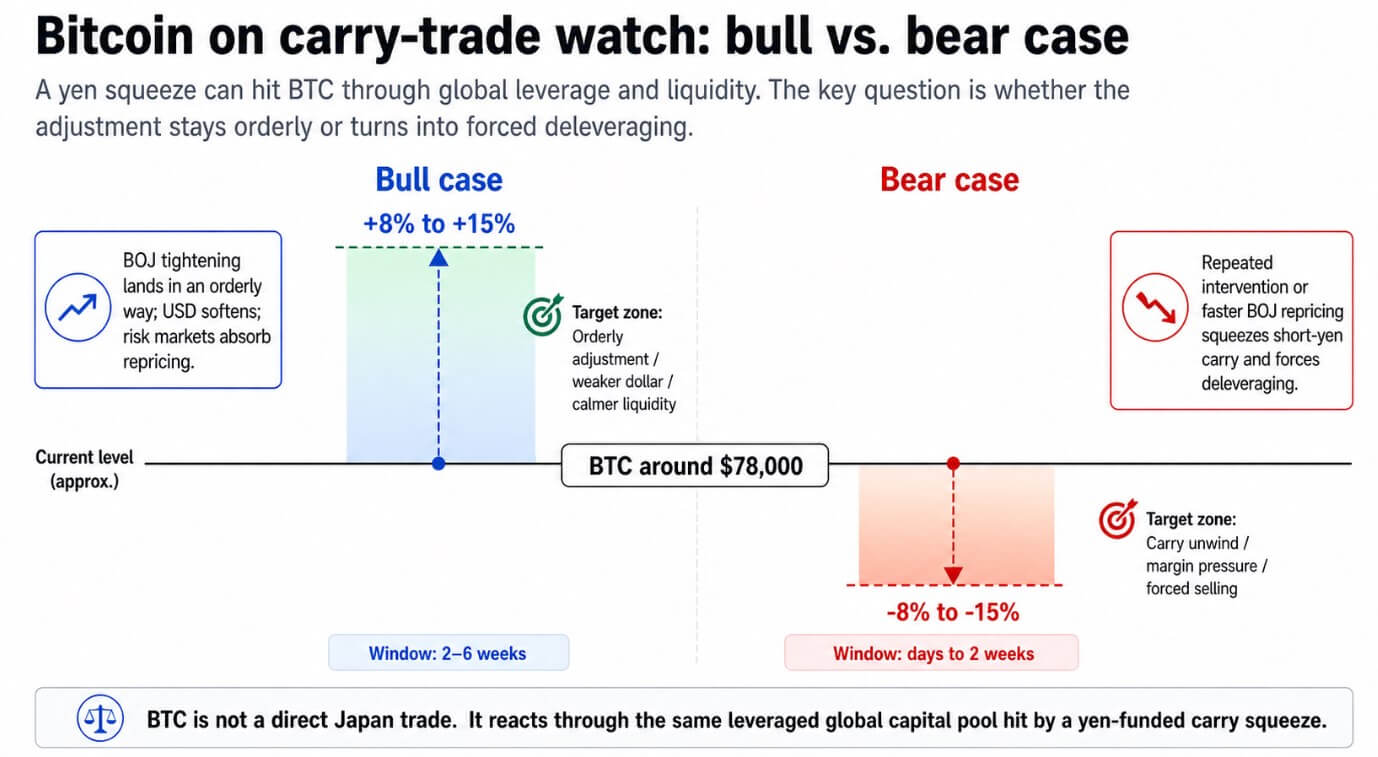

As of May 1, Bitcoin was trading within the $78,000 range and reached an intraday peak nearing $79,000. In scenarios where yen appreciation necessitates rapid deleveraging among leveraged macro portfolios, traders may resort to selling Bitcoin due to its liquidity—especially when it is held within portfolios requiring immediate cash infusions.

The Bullish Scenario: Potential Outcomes Following BOJ Actions

If dissenting opinions within the BOJ materialize into an actual rate hike in June, this would initiate a credible tightening cycle capable of compressing carry spreads and rendering fresh accumulations of short-yen positions less appealing. Consequently, such developments may exert downward pressure on the dollar’s value.

The intervention has already catalyzed a decline in the dollar index by approximately 0.8%, with concomitant gains observed across major currencies such as the euro, pound sterling, and Swiss franc. Historical trends indicate that such broad-based dollar depreciation creates a favorable backdrop for Bitcoin—a digital asset closely aligned with global dollar liquidity dynamics.

In an ideal scenario characterized by orderly adjustments following a June hike by the BOJ—devoid of disorderly unwinds—USD/JPY would stabilize within a tighter range while global risk markets would absorb necessary repricing without triggering cascading margin calls.

Under these conditions, Bitcoin could navigate initial volatility effectively and return to a regime characterized by weaker dollar and easier liquidity—factors which previously propelled its bullish trajectory through early-2024.

A recent outlook published by Coinbase Research for Q2 reveals that approximately 75% of institutional respondents perceive BTC as undervalued at prevailing levels—indicating robust buying interest poised to emerge following any transient dislocation in price dynamics.

A plausible outcome under this scenario could involve a recovery ranging from 8% to 15% over a two-to-six-week timeframe following stabilization efforts.

The Bearish Scenario: Risks Associated with Continued Intervention or Unexpected Policy Shifts

Conversely, persistent interventions or abrupt shifts in policy expectations concerning BOJ actions could precipitate significant pressure on short-yen trades—potentially leading to simultaneous Value-at-Risk (VaR) adjustments and margin reductions across macro portfolios.

In such circumstances, traders may opt to liquidate their Bitcoin holdings due to its liquidity profile—particularly if held within leveraged books facing mounting pressure.

The historical precedent set during August 2024 serves as an illustrative reference point; during this period traders experienced an approximate drawdown of 15% over mere days—a consequence driven by analogous carry mechanics compounded through forced selling measures.

The current trading level for Bitcoin at approximately $78,000 offers minimal cushion for holders benefiting from substantial embedded gains who may be reluctant or unable to endure further dips in valuation.

A drawdown within the range of 8% to 15% aligns closely with historical patterns observed when interventions recur absent substantive policy backing from monetary authorities.