preferred on

Overview of Regulatory Actions Against Peer-to-Peer Crypto Trading in the UK

The recent coordinated initiative by UK authorities represents a significant escalation in regulatory oversight concerning suspected illegal peer-to-peer (P2P) cryptocurrency trading. The operation sends an unequivocal message to market participants: once an individual engages in cryptocurrency transactions as a business, the expectation of compliance with regulatory frameworks—including identification, verification, record-keeping, and accountability—becomes paramount.

Regulatory Framework and Recent Actions

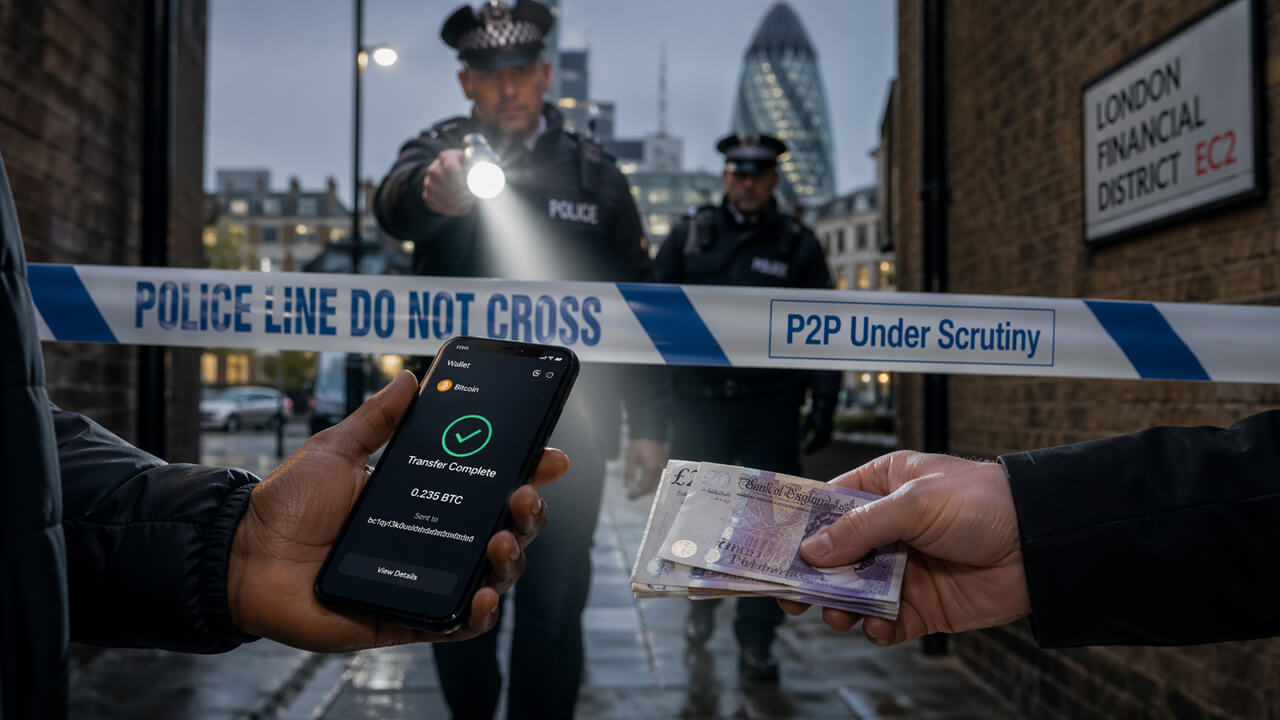

The Financial Conduct Authority (FCA) has collaborated with law enforcement and tax authorities to execute inspections at eight London locations associated with suspected illegal P2P cryptocurrency trading activities. Each site received cease-and-desist letters, and the evidence collected during these inspections is now serving as the foundation for ongoing criminal investigations. Notably, reports indicate that there are currently no FCA-registered P2P cryptocurrency traders operating within the United Kingdom.

The legal dichotomy between occasional cryptocurrency transactions among individuals and the operation of a systematic trading platform is clear. The threshold is crossed when individuals consistently exchange cryptocurrencies for fiat currency, facilitate such exchanges, or engage in the swapping of one cryptoasset for another as part of a business activity.

Anti-Money Laundering Regulations

The FCA’s stringent anti-money laundering (AML) regime explicitly categorizes “cryptoasset exchange providers,” inclusive of P2P platforms, as entities subject to regulatory oversight. Individuals engaged in repeated buying and selling of cryptocurrencies on behalf of others, advertising such services, handling customer funds, or acting as intermediaries cannot simply characterize their activities as informal.

Under the auspices of the UK’s Money Laundering Regulations, businesses involved in crypto activities that fall within the regulatory scope are mandated to register with the FCA prior to commencing operations; failure to do so constitutes a legal infraction.

Implications of Regulatory Enforcement

A registered cryptocurrency firm is obligated to perform customer due diligence, monitor transactions, maintain comprehensive records, and report any suspicious activities. These requirements form an integral component of a financial system designed to thwart illicit activities such as money laundering, terrorist financing, and fraud.

For the FCA, an unregistered P2P trading operation poses risks analogous to those presented by any unregulated money-services business: it can facilitate the conversion of illicit funds into usable assets while leaving minimal traceability.

Tax Compliance Issues

The involvement of tax officials in these investigations complicates matters further. While it does not automatically imply that every target has undeclared income or outstanding tax obligations, it illustrates how authorities perceive informal crypto services. A business that collects fees, generates spreads, or yields profits through repeated trading can create taxable income. If such a business concurrently eschews registration and customer verification protocols while maintaining opaque accounting practices, enforcement efforts will inherently encompass financial crime supervision, tax compliance monitoring, and consumer protection measures.

Regulatory Evolution in the UK Crypto Landscape

The UK has undertaken considerable efforts to integrate cryptocurrency operations into a structured regulatory framework over recent years. This transformation includes expanded FCA jurisdiction over stablecoin issuers and custodians and aims for full implementation of a comprehensive cryptoasset regime by October 2027 under Financial Services and Markets Act (FSMA)-style regulations.

Legal Recognition of Digital Assets

Moreover, clarity has been achieved regarding the classification of digital assets as a distinct category of personal property. This legal recognition provides courts with a robust framework for adjudicating issues related to ownership, recovery, custody, and insolvency disputes. Such recognition facilitates not only regulatory compliance but also empowers stakeholders when navigating incidents involving asset theft or platform failures.

The Tension Between Regulation and Crypto’s Original Promise

The intersection of recognition and regulation often leads to increased scrutiny from authorities. As the state acknowledges cryptocurrencies as legitimate property and market instruments, it concurrently seeks enhanced transparency regarding service providers’ identities and accountability in preventing criminal financial flows.

Bitcoin was initially conceived as a decentralized peer-to-peer electronic cash system; however, its surrounding market dynamics have evolved dramatically. Although users retain the ability to manage private keys and transact autonomously without intermediaries like banks or exchanges, large-scale access predominantly operates through regulated exchanges and custodians.

The Legal Distinction Between Holding Versus Trading Cryptocurrency

This paradigm creates a legal distinction that regulators can leverage effectively. While holding Bitcoin may be perceived as an individual right, operating a business that facilitates its exchange transforms this activity into one subject to regulatory oversight. The FCA’s actions against unregulated P2P services underscore this imperative.

Consequences for Market Dynamics

The implications of recent enforcement actions extend beyond legal compliance; they fundamentally reshape market dynamics for participants who did not initially intend to engage in illicit activities. As informal exchanges are systematically curtailed by regulatory pressure, an increasing volume of trading activity is migrating towards regulated platforms.

Benefits and Downsides of Regulated Platforms

– Enhanced recourse for consumers

– Improved transparency and disclosures

– Streamlined record-keeping

However:

– Increased identity verification processes

– Heightened transaction monitoring requirements

– Greater susceptibility to account freezes or access restrictions

The initial casualties in this regulatory landscape include privacy and accessibility for users who rely on informal routes into cryptocurrency markets. These channels often serve individuals facing challenges with traditional banking systems or lacking requisite documentation.

Furthermore, autonomy—the core tenet underpinning the crypto movement—is compromised as users become increasingly reliant on regulated intermediaries that may impose constraints reminiscent of traditional financial systems.

The UK’s regulatory environment mirrors global trends wherein jurisdictions are progressively transforming cryptocurrencies from contentious legal issues into structured operational frameworks characterized by specific rules governing issuers, exchanges, custody arrangements, payments, and consumer protection.

The FCA’s operations in London epitomize this global shift towards consolidating informal access points within established regulatory perimeters. While this transition may provide advantages for larger exchanges and registered entities—facilitating integration with traditional financial systems—it simultaneously diminishes the fundamental essence of peer-to-peer transactions.

The paradox remains: unregistered crypto dealings harbor tangible risks necessitating regulatory oversight; yet a framework that categorizes every instance of informal exchange as a commercial entity subject to monitoring stifles the direct financial interactions that originally imbued cryptocurrencies with cultural significance.

As we navigate this evolving landscape in the UK—and globally—the pressing question remains: what form will remain for cryptocurrency markets once safety protocols are enforced within the confines of surveillance-heavy frameworks? Efforts to enhance safety may inadvertently lead cryptocurrencies closer to resembling traditional financial systems they were initially designed to circumvent.