A senior official from the White House tasked with digital assets has issued a vehement critique of the traditional banking sector’s persistent resistance to the proposed yield-bearing stablecoin provisions encapsulated within the CLARITY Act.

On April 17, Patrick Witt, the Executive Director of the White House Presidential Advisory Committee on Digital Assets, leveled allegations of “greed or ignorance” against financial institutions, attributing their escalated lobbying efforts aimed at obstructing the implementation of yield-bearing stablecoins in forthcoming legislation to these motivations.

“It’s hard to explain any further lobbying by banks on this issue as motivated by anything other than greed or ignorance. Move on.”

Legislative Developments: Bipartisan Compromise on Stablecoin Yield

The unprecedentedly pointed rhetoric emanating from the administration underscores a burgeoning schism between the White House and Wall Street regarding the trajectory of the $320 billion stablecoin market.

Throughout the preceding year, the White House has exerted considerable effort to forge a consensus between the banking industry and the cryptocurrency sector; however, such endeavors have thus far proven fruitless.

The latest initiative, introduced by Senators Thom Tillis and Angela Alsobrooks, proposes a bipartisan compromise that seeks to prohibit passive yields on stablecoin holdings while simultaneously permitting activity-based rewards.

In contradiction to this proposal, unnamed banking trade associations have reportedly articulated concerns that even this constrained framework constitutes a fundamental threat to the integrity of the traditional financial system. As a result, they have intensified their lobbying campaigns targeting numerous senators within the Senate Banking Committee.

Notably, representatives from the American Bankers Association had previously asserted that potential loopholes regarding stablecoin yields in the CLARITY Act could precipitate an alarming $6.6 trillion in deposit outflows from conventional banks.

This dire forecast stands in stark contrast to data presented by the White House. A report disseminated by the Council of Economic Advisers posited that a comprehensive ban on stablecoin yields would impose an aggregate cost of approximately $800 million upon consumers. Furthermore, it contended that such a yield prohibition would do little to safeguard bank lending while also forgoing consumer advantages associated with competitive returns on stablecoin holdings.

Nevertheless, banking representatives have dismissed these analyses, maintaining that:

“As yield-paying payment stablecoins expand, households and businesses have stronger incentives to move funds out of bank deposits and into stablecoins unless Congress prohibits yield. Even if total deposits in the banking system remain constant, deposits will be reallocated away from smaller banks toward a smaller set of large institutions, and the share of deposits tied up in stablecoin reserves will eat into overall bank lending capacity.”

The Ascending Demand for Yield-Bearing Stablecoins

The legislative impasse unfolds against a backdrop characterized by rapid evolution within the market, wherein holders of stablecoins are increasingly gravitating toward yield-bearing assets.

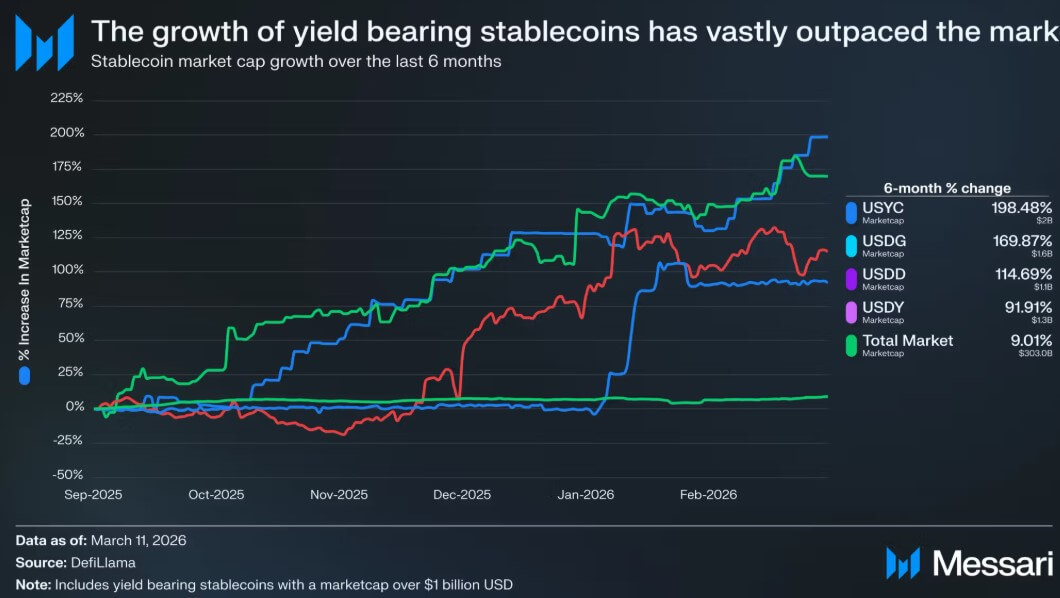

According to data from Messari, the proliferation of yield-bearing stablecoins has surged at a rate 15 times faster than that of the broader stablecoin market over the past six months.

This accelerated growth within the sector necessitates prompt action from legislators to reconcile existing disparities.

Senator Thom Tillis has indicated that deliberations regarding the compromise text are ongoing; meanwhile, Senator Angela Alsobrooks has suggested that an announcement regarding this matter may occur as early as next week.

However, should the Banking Committee fail to propagate this bill prior to the conclusion of April, political circumstances may render its passage improbable until 2026. In fact, Senator Cynthia Lummis has issued warnings that legislative approval might be postponed until as late as 2030 if a consensus is not achieved expeditiously.

The cryptocurrency sector remains steadfast in its assertion that yielding to banking sector pressures will effectively stifle domestic innovation.

Dan Spuller, Executive Vice President of Industry Affairs at the Blockchain Association, articulated this perspective succinctly: “Our industry is in the 11th hour of negotiations and the push to force everything into a bank model is real. Stablecoins are fully reserved payment tools, not deposit-taking institutions. If we get this right, America wins.”