Introduction to Form 1099-DA for Cryptocurrency Investors

The advent of the Form 1099-DA marks a significant milestone in the regulatory landscape governing cryptocurrency investments for U.S. taxpayers. As this new Internal Revenue Service (IRS) form rolls out, many investors are confronted with a fundamental challenge: the necessity to comprehend its implications prior to its receipt.

A comprehensive survey conducted by Coinbase and CoinTracker, encompassing a sample size of 3,000 U.S. cryptocurrency users, reveals a disconcerting trend. According to the findings, 61% of participants were oblivious to the new reporting regulations set to take effect in 2025. Notably, despite 74% acknowledging that cryptocurrency transactions can trigger tax liabilities, only 56% of respondents rated their understanding of cryptocurrency tax regulations as satisfactory or excellent. This disparity underscores a critical knowledge gap within the investor community.

Regulatory Framework and Reporting Requirements

The IRS is transitioning towards a more standardized reporting framework concerning digital asset transactions, necessitating brokers to report gross proceeds from digital asset sales via Form 1099-DA starting in 2025. Furthermore, basis reporting on covered securities is slated to commence in 2026.

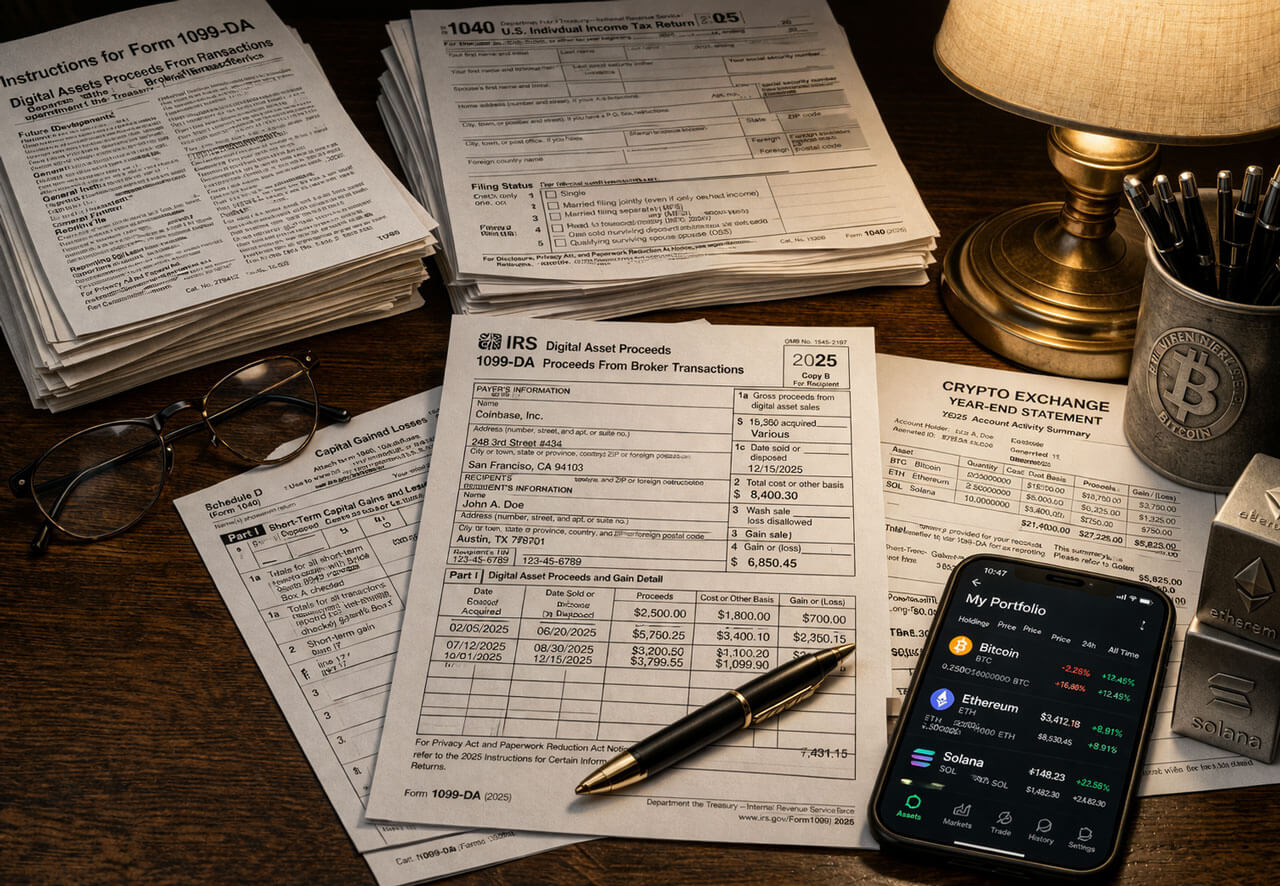

– **Understanding Form 1099-DA**:

– This form is instrumental for brokers in reporting proceeds from digital asset dispositions to both taxpayers and the government.

– It is essential to note that most statements issued in 2025 will omit basis information, which is crucial for accurately determining taxable gains or losses.

– Consequently, investors may misinterpret their financial standing based on incomplete data presented in these forms.

The IRS has explicitly articulated that all taxpayers are mandated to report income, gains, and losses associated with digital asset transactions irrespective of whether they receive Form 1099-DA. Moreover, they must independently calculate their basis before submitting their tax returns.

Interpreting Form 1099-DA: A Cautionary Perspective

As this inaugural filing season unfolds, the potential for misinterpretation of Form 1099-DA is heightened due to its transitional nature. For instance, a taxpayer who acquires Bitcoin on one exchange, subsequently transfers it into self-custody, and later sells a portion on a different platform may receive a Form 1099-DA indicating disposal proceeds. However, if the asset was transferred from another broker or self-custody wallet, the absence of basis information on the form complicates the accurate calculation of taxable outcomes.

Tax professionals contributing insights to *The Tax Adviser* caution that taxpayers may receive Forms 1099-DA devoid of basis information for assets transferred from alternate sources or for transactions conducted on non-custodial platforms. This necessitates a vigilant approach; taxpayers must not misconstrue this document as a comprehensive brokerage statement.

Jonathan Cutler, a senior manager at Deloitte, articulated this sentiment succinctly, asserting that while Form 1099-DA serves as an indicator of crypto transactions, it is imperative for taxpayers to maintain meticulous records of their activities. The IRS echoes this sentiment in its guidance, emphasizing that reliance solely on Form 1099-DA without supplementary records can lead to significant discrepancies in tax filings.

Common Pitfalls Among Investors

The findings from the Coinbase and CoinTracker survey illuminate pervasive misconceptions surrounding taxable events within the cryptocurrency ecosystem. Notably:

– Only 49% of respondents accurately identified that a tax event occurs upon the sale of cryptocurrency.

– A substantial proportion—41%—erroneously believed that tax liabilities trigger upon transferring assets to a bank account.

– Additionally, 36% opined that taxation applies only when profits exceed a specific threshold.

This lack of clarity persists despite the fact that users engaged with an average of 2.5 platforms or wallets; approximately 83% reported utilizing self-custodial solutions while 71% admitted to transferring assets between various wallets or platforms.

The IRS categorically classifies digital assets as property for federal income tax purposes. According to IRS guidelines regarding Form 1099-DA:

– Taxpayers may receive this form upon disposing of digital assets for fiat currency.

– The form is applicable when assets are exchanged for other digital currencies or utilized for goods and services.

Despite an overarching awareness that cryptocurrency may be subject to taxation among investors—76% acknowledged potential cost-basis adjustments—only 35% indicated having previously implemented such adjustments.

Shehan Chandrasekera, Head of Tax Strategy at CoinTracker, succinctly encapsulated the dilemma faced by investors: “While crypto brokerages will provide 1099-DA forms this tax year, users are responsible for correctly computing their cost basis, holding period and actual gains or losses. This cost basis issue is uniquely hard to solve.”

Increasing Visibility Amidst Compliance Challenges

The proactive reporting measures instituted by the IRS reflect an evolving recognition that prior systems inadequately captured the breadth of cryptocurrency market activity. A study published in *Review of Accounting Studies* (2026) utilizing IRS data indicated that the agency only observed between 32% and 56% of U.S. cryptocurrency holders.

Furthermore, an analysis conducted by the National Bureau of Economic Research (NBER) revealed that an alarming proportion—88%—of crypto holders failed to report their holdings or gains. Even amongst those utilizing domestic exchanges that provided identifiable data to tax authorities, approximately 80% neglected to declare their positions.

In light of intensified scrutiny from regulatory bodies, there is a discernible shift in investor behavior as they adapt their strategies in anticipation of compliance requirements. Preliminary observations during this inaugural season indicate that accountants are increasingly engaged in forensic reconciliation processes against client-maintained records rather than straightforward form matching.

For U.S. investors navigating this complex landscape during the current filing cycle, it is imperative to recognize that while Form 1099-DA provides enhanced visibility into many crypto transactions conducted in 2025, it does not unequivocally resolve tax obligations. Taxpayers remain responsible for substantiating acquisition costs, documenting asset movements, determining holding periods, and accurately assessing whether disposals resulted in gains or losses.

Until comprehensive records are reconciled effectively, there exists a risk that while governmental oversight may become more robust regarding sales data, individual investors may struggle to substantiate their reported profits adequately.