Analysis of Recent Geopolitical Developments and Their Impact on Bitcoin and Global Markets

In a recent strategic engagement, Senator Marco Rubio conveyed to G7 foreign ministers the potential for the ongoing conflict with Iran to extend over the next two to four weeks. This information has significant implications for Washington’s closest allies and the broader financial markets, effectively initiating a countdown that could influence market dynamics considerably.

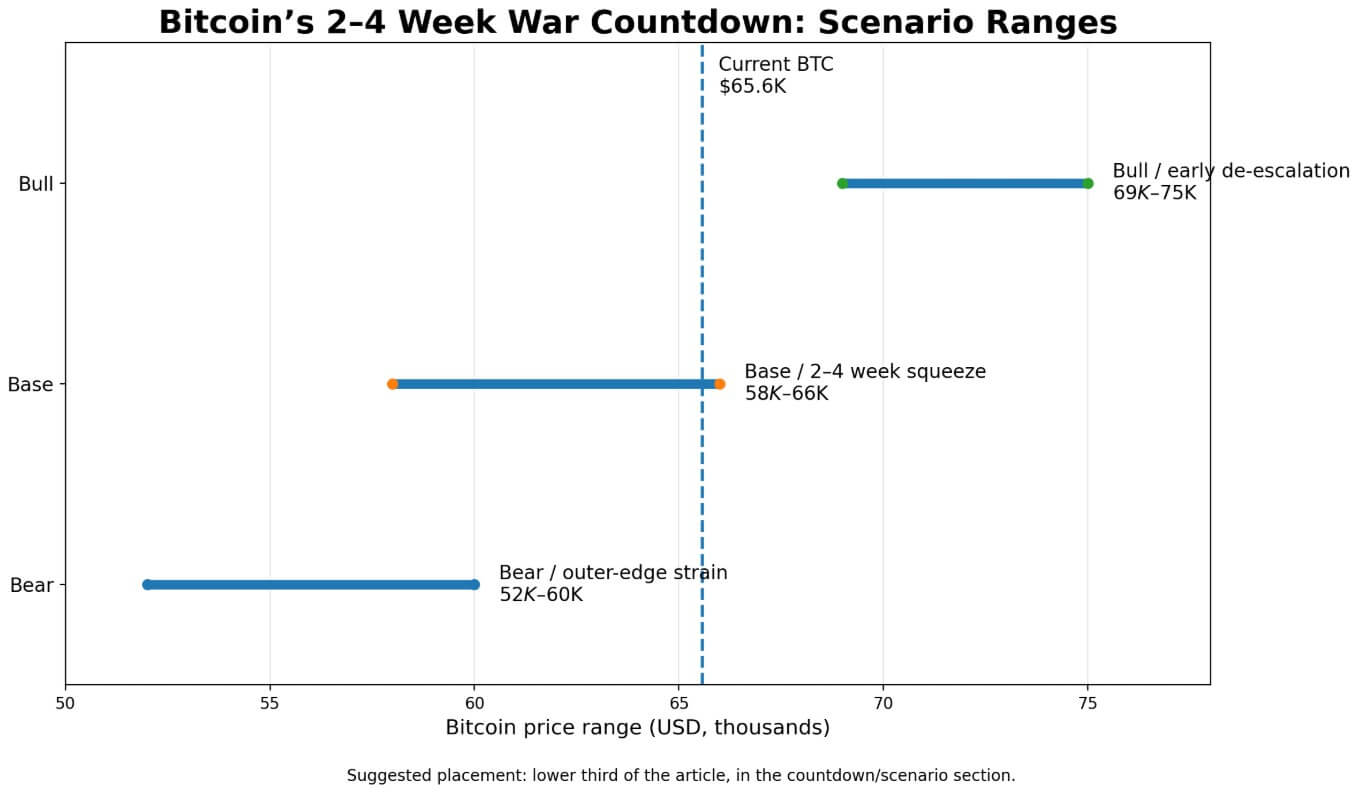

Publicly, Rubio articulated that the military operation should conclude in “weeks, not months.” The disparity between these two timelines presents a critical window that could sustain macroeconomic pressures, particularly affecting Bitcoin’s trading behavior. On March 27, Bitcoin recorded an intraday low of $65,571.07, reflecting a decline of approximately 4.4% for the day. Concurrently, Brent crude oil prices surged to $111.52 per barrel, marking a staggering increase of 53% since the onset of hostilities on February 27.

The current market landscape is further characterized by significant movements in other key financial indicators: the Nasdaq Composite Index has entered correction territory, the yield on the U.S. 10-year Treasury note stands at 4.44%, and futures markets indicate a virtually zero probability of any Federal Reserve rate cuts occurring within this fiscal year. This confluence of events elucidates the precise factors contributing to Bitcoin’s recent losses.

| Asset / Indicator | Latest Level / Status | Move / Context |

|---|---|---|

| Bitcoin (BTC) | $65,571.07 | Down ~4.4% on Mar. 27 |

| Brent Crude | $111.52 | Up 53% since Feb. 27 |

| Nasdaq Composite | Correction Territory | Risk Assets Under Pressure |

| U.S. 10-Year Treasury Yield | 4.44% | Higher Yields Tightening Financial Conditions |

| Fed Futures | ~0% Probability of a Rate Cut This Year | Markets Pricing a Rate-Cut Freeze |

The Transmission Mechanism of Geopolitical Tensions on Market Dynamics

The escalation of oil prices above $100 per barrel exerts upward pressure on freight costs across various supply chains globally. Data from the U.S. Energy Information Administration (EIA) indicates that tanker rates for Very Large Crude Carriers (VLCCs) operating between the Middle East and Asia reached their highest levels since at least November 2005 as of March this year. This situation is likely to engender persistently high inflation expectations, as evidenced by the University of Michigan’s consumer sentiment index declining to 53.3 and one-year inflation expectations rising from 3.4% to 3.8%.

Federal Reserve Governor Lisa Cook has articulated that the conflict in Iran has shifted the risk balance toward inflationary pressures, thereby solidifying the rationale for maintaining a freeze on interest rate cuts—an action that invariably channels through to Bitcoin’s pricing dynamics.

The cryptocurrency has increasingly come to be regarded as a high-beta liquidity asset. Research conducted by the International Monetary Fund (IMF) has documented that Bitcoin exhibits a higher correlation with equities than with traditional safe-haven assets such as gold, bonds, or major fiat currencies.

A study published in Finance Research Letters in 2024 found that Bitcoin’s returns and volatility are particularly responsive to political uncertainty shocks, especially during periods characterized by financial stress. The current decline in Bitcoin’s price is attributable to sustained geopolitical tensions which prolong the oil supply shock and maintain tight liquidity conditions.

The Implications of Duration on Market Pricing Strategies

Market participants are now actively pricing in the duration of the conflict, interpreting each military or diplomatic development as a data point indicative of a longer repricing cycle. The Intercontinental Exchange (ICE) has recorded unprecedented crude trading volumes and open interest levels through March, signaling ongoing adjustments in market perceptions.

Historical context further illustrates this point: when President Donald Trump postponed strikes on Iranian energy infrastructures and de-escalation hopes emerged, global equity funds attracted inflows totaling $37.77 billion in the week ending March 25. Conversely, when Iran refuted discussions and ceasefire prospects diminished, equity valuations experienced a downturn.

The market oscillates based on prevailing perceptions regarding the duration of energy shocks; Rubio’s private timeline has shifted expectations toward a prolonged scenario.

Scenario Analysis: Considering Potential Outcomes

Looking ahead to potential outcomes within this timeframe, an optimal scenario would involve diplomatic resolutions that facilitate normalization within approximately seven to ten days. Such an outcome would likely see Brent crude prices retreating towards the $95-$110 range while mitigating inflation expectations and reducing narratives around sustained market cuts into 2026.

Goldman Sachs posits that clarity surrounding military operations’ cessation would rapidly diminish oil risk premiums. In this favorable context, Bitcoin could rebound swiftly, potentially reaching price levels between $69,000 and $75,000—supported by easing post-disruption forecasts from EIA and rapid re-entry from equity funds during prior de-escalation phases observed in late March.

Conversely, a grim scenario arises if hostilities persist towards the outer limit of Rubio’s four-week estimate. In this case, friction within Hormuz continues unabated; war-risk insurance rates remain elevated; and no credible ceasefire emerges—resulting in Brent crude stabilizing within a $110-$135 range consistent with Goldman’s March-April projections and Reuters’ average under prolonged disruptions.

This environment would sustain uncomfortable inflation levels while leaving the Federal Reserve sidelined; thus leading Bitcoin’s price to hover between $58,000-$66,000 due to continuous pressure from liquidity constraints established since February 27.

The academic literature supports this framing over any instinctual safe-haven narrative associated with cryptocurrencies during geopolitical crises. A study published in 2025 concluded that traditional hedges against geopolitical risks—such as gold, the U.S. dollar, and oil—exhibit more reliable protective qualities compared to cryptocurrencies across varying risk environments.

In essence, should tensions persist beyond two to four weeks without resolution, it will likely lead to at least one additional inflation print, another Federal Reserve meeting without rate adjustment decisions, and continued elevated freight and energy costs before any substantive macroeconomic clarity can be attained.

This period of duration encapsulates critical conditions wherein elevated oil prices coincide with an absence of anticipated rate cuts—two essential components driving liquidity ceilings across risk assets like Bitcoin.

The bullish case hinges upon an expeditious resolution that reopens liquidity pathways while reversing price compressions; conversely, bearish scenarios suggest continued constraints validating underlying liquidity dynamics governing Bitcoin’s recent performance since February.

Market participants are already factoring in these timelines without adequately integrating more optimistic prospects into their analyses.