Bitcoin Market Dynamics in the Context of Recent Macro Events

The recent volatility observed in Bitcoin’s price trajectory can be attributed to a confluence of macroeconomic factors, including an oil price shock, escalating Treasury yields, the retraction of anticipated rate cuts, and a significant expiry of derivative contracts on the Deribit exchange. This complex interplay has culminated in a substantial downward adjustment in Bitcoin’s valuation.

Impact of Derivative Expiry on Market Sentiment

On March 27, approximately $14.1 billion in Bitcoin (BTC) options were poised for expiration, alongside an additional $2.2 billion in Ethereum (ETH) contracts, bringing the aggregate total to approximately $16.38 billion. Notably, this figure represents nearly 40% of Deribit’s open interest in BTC rolling off in a singular session—a substantial event with implications for market stability.

According to reports by Reuters, the prevailing risk-off sentiment has been exacerbated by oil prices surging above $105 per barrel, heightened Treasury yields, and a strengthening U.S. dollar. Concurrently, market participants have adjusted their expectations regarding Federal Reserve rate cuts for 2025 amidst increasing geopolitical tensions in the Middle East.

As of yesterday, Bitcoin recorded an intraday low of $68,127, with Ethereum experiencing a decline to $2,036. The timing of the expiry coincides with an ongoing sell-off, pushing Bitcoin’s value down to approximately $66,200 this morning and Ethereum below the $2,000 threshold.

The Significance of the Last 30 Minutes Before Expiry

The settlement mechanism employed by Deribit for expiring contracts is particularly noteworthy. Contracts are settled at 08:00 UTC using a 30-minute time-weighted average price (TWAP) derived from observations sampled every four seconds between 07:30 and 08:00 UTC. This approach generates approximately 450 data points rather than relying on a single closing print, rendering the delivery price less susceptible to manipulation while simultaneously allowing broad market movements during this interval to directly influence settlement outcomes.

During this critical window, the delta of expiring options and futures experiences linear decay towards zero. As hedges are adjusted and positions rolled over, the pricing clock is actively ticking down. This unique convergence attracts disproportionate attention relative to its brief duration.

A scholarly paper published in 2025 utilizing Deribit data indicated that BTC options activity tends to cluster around the hours of 8:00 – 9:00 GMT, with the settlement-hour effect being most pronounced on days characterized by numerous expiring contracts and shorter maturities—conditions that are applicable in this instance.

| Metric | Value | Significance |

|---|---|---|

| BTC options expiring | $14.16B | Magnitude of Friday’s expiry |

| ETH options expiring | $2.22B | Contributes to overall market impact |

| Combined BTC + ETH expiry | $16.38B | Total scale of market reset |

| Share of Deribit BTC open interest rolling off | Nearly 40% | Highlights concentration risk within one session |

| Settlement time | 08:00 UTC, March 27 | A fixed event for market observers |

| Key pricing window | 07:30–08:00 UTC | This period determines the delivery price |

| Settlement method | 30-minute TWAP of Deribit index | The final price is based on an average rather than a single print |

| Sampling frequency | Every 4 seconds | Generates approximately 450 observations |

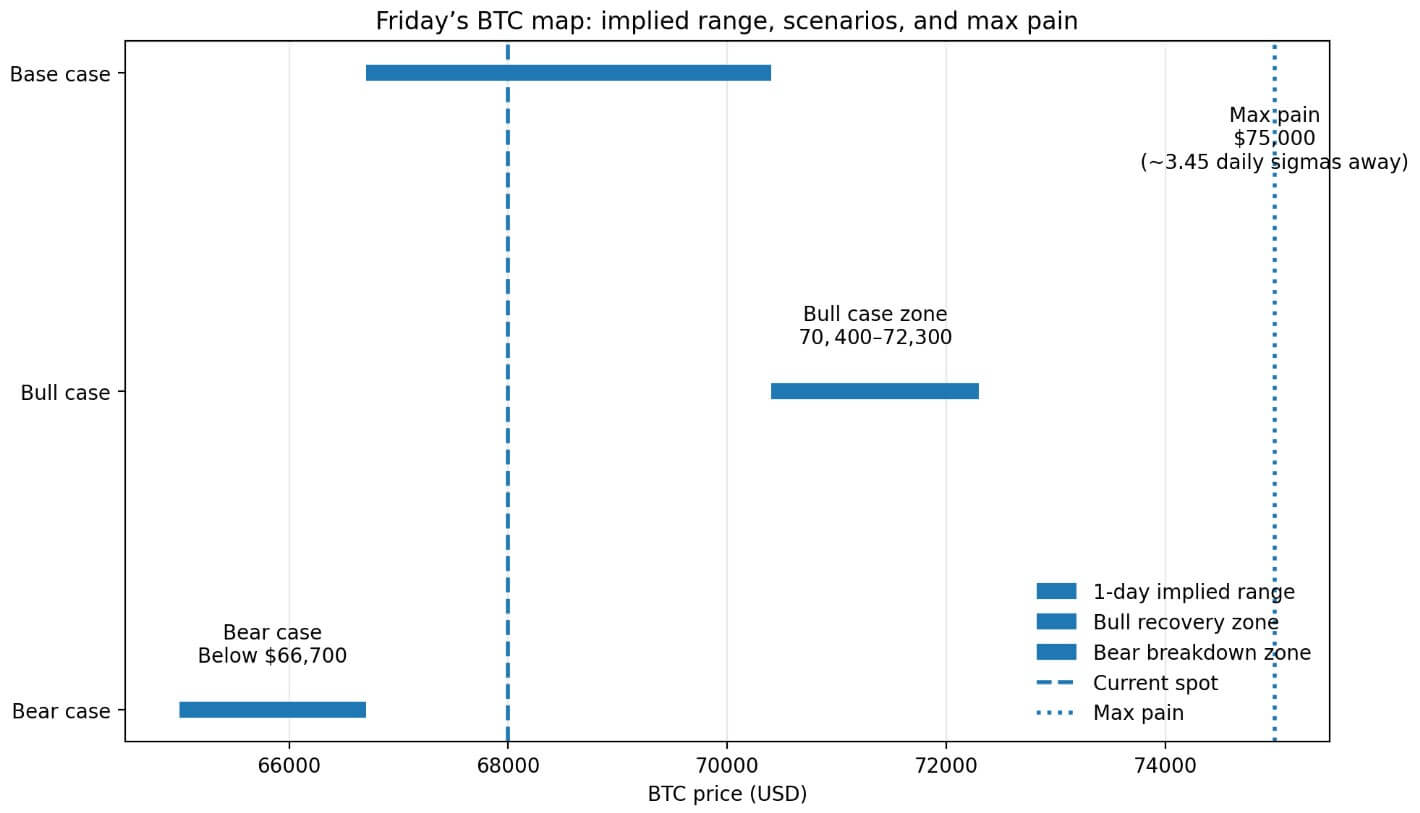

| BTC spot reference price | Near $68,000 | Benchmark for all comparative analyses |

| BTC max pain level | $75,000 | A reference point for positioning rather than a forecast |